.png)

Understanding Workers’ Compensation and Employer Liability Insurance: What Every Business Needs to Know

If you run a business and have employees, chances are you’ve already felt the pressure of making sure everyone (and everything) is properly protected. Between the legal requirements and the real-life risks of running a workplace, understanding your insurance coverage isn’t just another checkbox.

Two of the most important policies every business owner should know about are workers’ compensation insurance and employers’ liability insurance. They often get grouped together, but they’re not the same thing. Each plays a different role in protecting your business and your team when something goes wrong.

In this article, we’re going to break down the key differences, explain why these coverages matter, and walk you through things like how to get a workers’ compensation insurance certificate and how a PEO can make the process easier (and often, more affordable).

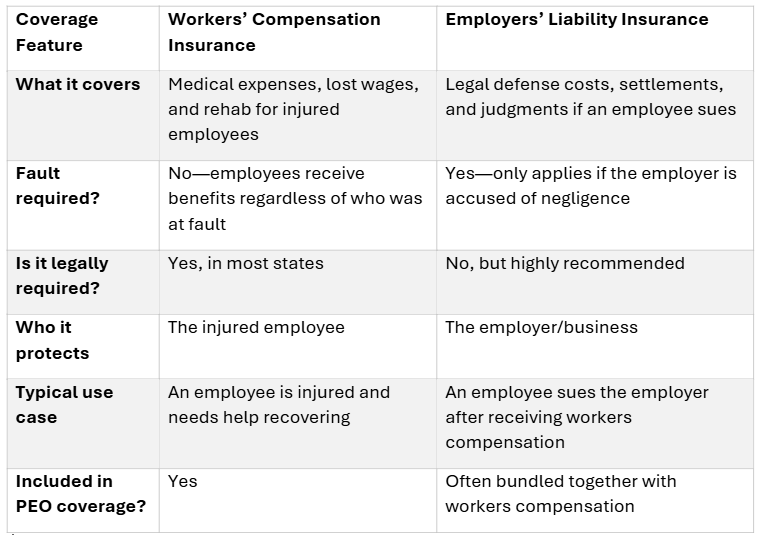

What Is Workers’ Compensation Insurance?

It is designed to protect both your business and your employees when the unexpected happens on the job. If someone gets hurt or becomes ill due to a work-related incident, this insurance helps cover their medical bills, lost wages, and rehabilitation, so they can recover without the added stress of financial worry.

For you as the employer, workers’ compensation insurance isn’t just helpful, it’s legally required in most states. It protects your business from certain lawsuits and ensures your team gets the care they need if something goes wrong.

Here’s a simple example: Let’s say an employee falls off a ladder and breaks their arm. Workers’ compensation would step in to pay for the emergency room visit, follow-up care, and even part of their missed income while they heal. Instead of that cost falling entirely on your shoulders, you’re covered, and your team knows they’re taken care of.

It’s about being a responsible employer, building trust with your team, and having a safety net when things don’t go according to plan.

Want to explore the topic further? Investopedia offers a detailed explanation of workers' compensation insurance, including how it works and who it protects. Check out the article here.

What Is Employers Liability Insurance?

While workers’ compensation insurance handles the basics like medical bills and wage replacement, there are times when it doesn’t cover everything. That’s where employers’ liability insurance comes in.

Think of it as an extra layer of protection for your business. If an employee gets hurt and decides to sue you for negligence (maybe they think you didn’t provide proper training or failed to maintain a safe work environment), employers’ liability insurance can help cover the legal costs, settlements, or judgments that could follow.

Here’s a real-world example: Imagine an employee is injured on the job and receives workers’ compensation benefits. But then they also file a lawsuit claiming your business was directly responsible for their injury, maybe due to unsafe equipment or lack of safety protocols. That’s where employers’ liability insurance steps in. It helps pay for your legal defense and any court-ordered payouts, so one incident doesn’t snowball into a financial crisis.

It’s not always required by law as workers’ compensation is, but it’s a smart (and often affordable) addition, especially if you want to be fully covered from all angles.

Together, these two policies (workers’ compensation insurance and employers’ liability insurance) form a solid foundation for protecting your business and your team.

Still curious about how employers' liability insurance works? Check out this in-depth overview from Investopedia for a deeper look at what it covers and why it matters: Read the full article here.

Employers Liability Insurance vs Workers Compensation

Want to dive deeper into how workers compensation insurance compares to other types of business coverage? Check out this helpful guide from The Hartford on the differences between general liability and workers’ compensation: Read more here.

It is important to understand that workers’ compensation insurance and employers’ liability insurance are not interchangeable, they work together. Workers’ compensation covers the immediate needs of injured employees, while employers’ liability steps in if legal action follows. Having both in place ensures that everyone is protected, from your team members to your bottom line.

Common Mistakes Businesses Make and How to Avoid Them

When it comes to protecting your team and staying compliant, even well-meaning business owners can overlook a few important details. Here are some of the most common mistakes we see and how to avoid them:

Assuming One Policy Covers Everything

It’s a common misunderstanding: you have workers compensation, so you’re fully covered, right? Not always. If an employee decides to sue your business for negligence, workers’ compensation will not cover your legal defense. That’s why pairing it with employers’ liability insurance is so important, they work together, not in place of each other.

Not Keeping Up with State-Specific Rules

Workers’ compensation laws vary depending on where your employees work. If you’re operating in more than one state (or even thinking about expanding), your coverage needs to reflect those differences. Otherwise, you could face fines or compliance issues.

Letting Your Workers’ Compensation Insurance Certificate Lapse

Some businesses forget to update or renew their certificate and that can cause major delays when bidding on projects, working with vendors, or passing inspections. Always keep an up-to-date workers’ compensation insurance certificate on file and ready to share.

Overpaying Because You Didn’t Shop Around

Rates for workers’ compensation and liability insurance can vary significantly depending on your industry, claims history, and provider. Many businesses unknowingly pay more than they need to, especially if they’re not working with a partner who can compare options on their behalf.

How to Obtain a Workers’ Compensation Insurance Certificate

This document is often required when working with contractors, applying for licenses, bidding on projects, or simply staying compliant with state regulations.

The good news? Getting one is usually a simple process:

- Find an expert

You’ll either work directly with an insurance carrier or partner with a Professional Employer Organization (PEO) that will find the best workers’ compensation plans for your business.

- Submit basic business information

You’ll provide details like your business name, number of employees, job roles, and payroll estimates. This helps determine your risk classification and policy rate.

- Purchase your policy

Once everything is reviewed and finalized, your policy becomes active, and you’re covered.

- Receive your workers compensation insurance certificate

After the policy is in place, your provider or PEO will issue the certificate. It’s usually a one-page document that includes your business info, coverage dates, and policy number.

This certificate isn’t something you want to overlook. Having it ready and up to date can help you avoid project delays, legal issues, or potential fines.

The Role of PEOs in Managing Workers’ Comp and Liability Insurance

Managing workers’ compensation and employers’ liability insurance on your own can get complicated fast, especially if your business is growing or operating in multiple states. That’s where a PEO (Professional Employer Organization) can make a big difference.

When you partner with a PEO, you’re essentially getting a team of HR, compliance, and insurance experts bundled into one solution.

Here’s what that really means:

Bundled Coverage That Simplifies Everything

Most PEOs include both workers’ compensation and employers’ liability insurance as part of their service offering. Instead of juggling multiple policies, providers, and deadlines, everything is handled through a single point of contact saving you time and reducing the chance of something slipping through the cracks.

Better Rates Through Group Purchasing

Because PEOs broker many businesses at once, they’re able to negotiate insurance rates as part of a larger risk pool. That often means you can access more affordable coverage than if you went shopping for a policy on your own.

Compliance Support and Risk Management

State laws around workers’ compensation and liability can be confusing and they’re constantly changing. PEOs stay on top of those regulations, so you don’t have to. Many also provide workplace safety training, employee handbook support, and guidance on how to reduce risks that lead to claims.

Help With Certificates and Claims

Need a workers’ compensation insurance certificate fast? Inclusive PEO can generate and send it to you. In the event of a claim, your PEO will guide you through the process and coordinate directly with the insurance provider, helping to ensure everything is handled quickly and correctly.

Conclusion: Protect Your People, Protect Your Business

Understanding the difference between workers’ compensation insurance and employers’ liability insurance isn’t just about checking off a legal requirement, it’s about building a safer, smarter business.

Workers’ compensation ensures your employees are supported when accidents happen. Employers’ liability insurance gives you peace of mind if a claim turns into a lawsuit. Together, they form the foundation of a responsible risk management strategy.

But here’s the other good news: you don’t have to figure it all out on your own.

At Inclusive PEO Brokers, we specialize in helping you find the right plan for your business. One that not only offers the coverage you need but also supports your operations and growth goals. We walk with you through every step, from evaluation to implementation and beyond.

Reach out today for a consultation and discover how the right PEO can protect your people, your business, and your peace of mind.

Sources:

Business News Daily: https://www.businessnewsdaily.com/10670-what-is-workers-compensation.html

.svg)

Seeking a different solution? Meet Your Business Needs