.png)

PEO Tax Compliance Explained for Business Owners

PEO tax compliance is defined as the process by which a Professional Employer Organization (PEO) acts as the employer of record for tax purposes, taking on responsibility for payroll tax withholding, deposits, and filings on behalf of your business. This arrangement operates through a co-employment model, where the PEO and your company share legal and administrative employer duties. The IRS recognizes the PEO as the filing entity, meaning W-2 forms carry the PEO’s name and Employer Identification Number (EIN). For small and medium business owners, this structure removes one of the most error-prone and penalty-heavy obligations in running a company.

How does the PEO co-employment model affect tax compliance?

The co-employment model splits employer responsibilities into two distinct roles. The PEO becomes the legal and tax employer, handling payroll processing, tax withholding, and government filings. You, as the client business, remain the worksite employer, retaining full control over hiring decisions, daily management, and employee performance.

This division matters because it directly determines who is accountable to the IRS and state tax agencies. The PEO files under its own EIN, which means your business is shielded from direct filing liability as long as the PEO performs its duties correctly. That protection is significant for founders managing their first hire or scaling a team across multiple states.

The legal framework governing this relationship is the client service agreement (CSA). This contract defines exactly which tax and administrative duties the PEO assumes and which remain with you. Reading the CSA carefully before signing is not optional. It is the document that determines your exposure if something goes wrong.

Here is what the PEO typically handles under the co-employment structure:

- Payroll tax withholding from employee wages each pay period

- Federal tax deposits to the IRS on the required schedule

- Form 941 filings (quarterly federal payroll tax returns)

- W-2 issuance to employees at year-end, under the PEO’s EIN

- State income tax withholding and remittance to each applicable state

- State unemployment insurance (SUI) filings and payments

Pro Tip: Ask your PEO to provide a copy of each Form 941 after it is filed. This gives you a paper trail and confirms filings are happening on schedule.

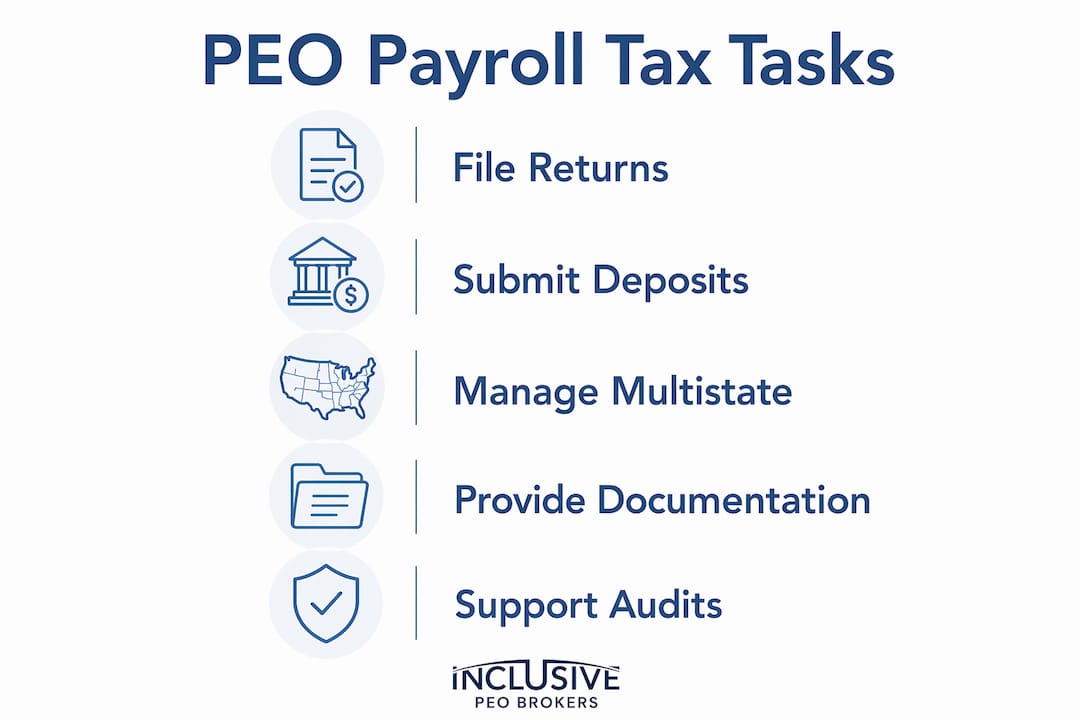

What payroll tax tasks does a PEO manage for you?

PEOs handle the full cycle of payroll tax compliance, from the moment you run payroll to the moment the IRS confirms receipt. Understanding this cycle helps you know what to verify and when.

Here is the typical sequence of payroll tax compliance tasks a PEO manages:

- Collect payroll data from your business, including hours worked, salaries, bonuses, and deductions.

- Calculate withholding amounts for federal income tax, Social Security, Medicare (FICA), and applicable state taxes.

- Remit withheld taxes to the IRS and state agencies on the required deposit schedule (semi-weekly or monthly, depending on your payroll size).

- File Form 941 quarterly to report wages paid and taxes withheld.

- File state unemployment tax returns on the schedule required by each state where employees work.

- Issue W-2 forms to all employees by January 31 each year, reporting annual wages and withholding.

- Reconcile annual filings with Form W-3, the transmittal form sent to the Social Security Administration.

The PEO files all required employment tax returns, including federal Form 941, annual W-2 reports, and state unemployment tax filings, on your behalf. Missing any one of these deadlines triggers IRS penalties that compound quickly.

Multistate compliance is where PEOs deliver the most value for growing businesses. Each state has its own unemployment tax rate, income tax withholding rules, and filing deadlines. Managing this manually for even two or three states is a significant administrative load. A PEO with multistate experience absorbs that complexity entirely.

| Filing | Frequency | Filed By |

|---|---|---|

| Form 941 | Quarterly | PEO (under its EIN) |

| W-2 Forms | Annually (by Jan. 31) | PEO (under its EIN) |

| State Unemployment Tax | Quarterly (most states) | PEO |

| State Income Tax Withholding | Per pay period | PEO |

| Form W-3 | Annually | PEO |

Your responsibility in this process is to provide accurate, timely payroll data. If you report incorrect hours or miss a bonus payment, the PEO cannot file correctly. Garbage in, garbage out applies here just as much as anywhere in finance.

How does PEO compliance support protect small business owners?

PEO compliance expertise protects businesses from fines and penalties tied to payroll tax law and reporting requirements. This protection is one of the primary reasons small business owners engage PEOs in the first place.

The financial exposure from payroll tax errors is real. The IRS charges a failure-to-deposit penalty ranging from 2% to 15% of the unpaid amount, depending on how late the deposit is. For a business with a $50,000 quarterly payroll tax liability, a late deposit can cost thousands of dollars in penalties alone.

Beyond direct tax penalties, PEOs also manage:

- Workers’ compensation compliance, including policy administration and audit support

- Unemployment insurance, including claims management and rate monitoring

- Benefits compliance, covering ACA reporting requirements and ERISA obligations

- New hire reporting, which is required by federal and state law within days of a hire

- Wage and hour compliance, helping you avoid misclassification and overtime violations

PEOs administer insurance coverage and provide compliance monitoring as part of co-employment agreements. That bundled approach means you are not managing separate vendors for workers’ comp, payroll, and HR compliance. Everything runs through one relationship.

Pro Tip: Review your CSA to confirm the PEO carries errors and omissions (E&O) insurance. If the PEO makes a filing error, E&O coverage determines whether you are protected from the resulting penalty.

PEO fees typically bundle payroll execution, workers’ comp, HR advisory, and compliance tracking, often making PEOs more cost-effective than purchasing separate solutions. For a 10-person company, the math usually favors the PEO by a wide margin.

What should you know about PEO compliance reporting?

Compliance reporting is the part of PEO tax compliance that most business owners underestimate. The PEO files on your behalf, but you remain responsible for verifying that filings are accurate and timely. Passive trust is not a compliance strategy.

Regularly reviewing compliance reports and payroll tax documentation from your PEO helps catch errors early and avoids penalties or audit complications. Most PEOs provide a client portal or dashboard where you can access payroll registers, tax deposit confirmations, and filed returns.

Here is what to monitor on a regular basis:

- Payroll registers after every pay run, confirming gross pay, withholding, and net pay match your records

- Tax deposit confirmations showing the IRS or state agency received funds on the correct date

- Quarterly Form 941 copies to verify wages reported match your internal payroll totals

- W-2 drafts in December, before they are issued, to catch any employee data errors

- State unemployment rate notices, which the PEO should forward to you each year

The table below compares what your PEO handles versus what you need to monitor yourself:

| Responsibility | PEO Handles | You Verify |

|---|---|---|

| Payroll tax deposits | Yes | Confirm deposit dates and amounts |

| Form 941 filing | Yes | Review copy for accuracy |

| W-2 issuance | Yes | Approve employee data before filing |

| State unemployment filings | Yes | Check rate notices annually |

| Payroll data input | No | You provide accurate data each period |

| Employee classification | Shared | Confirm classifications are correct |

Common red flags to watch for include unexplained changes in your tax deposit amounts, W-2 forms with incorrect Social Security numbers, or state notices arriving at your address rather than the PEO’s. Any of these signals a breakdown in the process that needs immediate attention.

If you are ever subject to an IRS audit, your PEO should provide complete documentation of all filings and deposits. Confirm this support is written into your CSA before you need it.

Key takeaways

A PEO acts as the legal employer of record for tax purposes, managing payroll tax filings, deposits, and compliance reporting while your business retains control of day-to-day employee management.

| Point | Details |

|---|---|

| PEO is the tax employer | The PEO files under its own EIN, handling Form 941, W-2s, and state filings on your behalf. |

| CSA defines your protection | Your client service agreement outlines which tax duties the PEO owns and which remain with you. |

| Multistate compliance is covered | PEOs manage varying state tax rates, deadlines, and filings across all states where you employ workers. |

| You must verify, not just trust | Review payroll registers, tax deposit confirmations, and quarterly filings regularly to catch errors early. |

| Bundled compliance saves money | PEO fees covering payroll, workers’ comp, and compliance tracking typically cost less than separate vendor solutions. |

What i have learned about PEO tax compliance after 133 implementations

The biggest misconception I see from small business owners is that signing with a PEO means tax compliance is fully off their plate. It is not. The PEO handles the execution. You are still responsible for the accuracy of the data you provide and for verifying the work gets done.

The second mistake I see regularly is skipping a thorough CSA review. Business owners are often eager to get started and treat the contract as a formality. That contract is the only document that determines your liability if the PEO misses a filing. Know what it says before you sign.

One thing that genuinely surprises founders is how much multistate complexity a PEO absorbs. I have worked with companies that hired their second employee in a different state and had no idea they had just created a new tax registration obligation. The PEO handled it without the founder even knowing it was an issue. That kind of quiet protection is hard to quantify but very real.

My practical advice: treat your PEO relationship like a financial partnership, not a vendor transaction. Schedule a quarterly review with your PEO contact to go over filings, confirm deposit records, and flag any upcoming changes in your workforce. That 30-minute conversation can prevent a $10,000 penalty.

— John

How inclusive PEO brokers helps you get PEO tax compliance right

Choosing the wrong PEO creates compliance gaps that cost you money and time. Inclusive PEO Brokers specializes in matching small and medium businesses with PEOs that fit their specific tax, payroll, and HR needs. With 133 successful implementations and an average client time savings of 80 hours in the selection process, the team knows which PEOs deliver on compliance and which ones fall short.

Whether you are making your first PEO selection or planning a PEO exit strategy that keeps your tax filings intact, Inclusive PEO Brokers guides you through every step. Visit Inclusive PEO Brokers to book a free consultation and get matched with the right PEO for your business.

FAQ

What is PEO tax compliance?

PEO tax compliance refers to the process by which a PEO, acting as the employer of record, manages payroll tax withholding, deposits, and government filings on behalf of a client business. The PEO files under its own EIN, covering federal and state obligations including Form 941 and W-2 reporting.

Who is legally responsible for payroll taxes in a PEO arrangement?

The PEO assumes legal responsibility for filing and remitting payroll taxes as the co-employer, but the client business remains responsible for providing accurate payroll data and verifying that filings occur correctly. Your client service agreement defines the exact division of liability.

Does a PEO handle multistate payroll tax compliance?

Yes. PEOs manage state income tax withholding, state unemployment insurance filings, and new hire reporting across every state where your employees work. This is one of the strongest compliance advantages for businesses with remote or distributed teams.

What happens to tax compliance when you leave a PEO?

Transitioning out of a PEO requires advance planning to address open tax filings, state registrations, and benefit terminations. You will need to establish your own EIN-based payroll setup and confirm all prior period filings are complete before the transition date.

How do i verify my PEO is filing taxes correctly?

Request copies of each Form 941 after filing, review tax deposit confirmations in your client portal, and reconcile W-2 drafts against your internal payroll records before year-end. Regular monitoring catches errors before they become IRS notices.

Recommended

.svg)

Seeking a different solution? Meet Your Business Needs