.png)

PEO Benefits Broker Comparison Guide for 2026

A PEO benefits broker comparison guide is the decision framework small business owners and HR managers use to evaluate whether a Professional Employer Organization or a standalone benefits broker best fits their workforce needs. These two models solve different problems. A PEO like ADP TotalSource or Justworks bundles payroll, compliance, and benefits under a co-employment model. A benefits broker like those at Nava Benefits or TBC Benefits Group focuses on plan selection and carrier access without taking on employer status. Choosing the wrong model costs you money, control, and time. This guide gives you the tools to choose correctly.

What are the key differences between peos and benefits brokers?

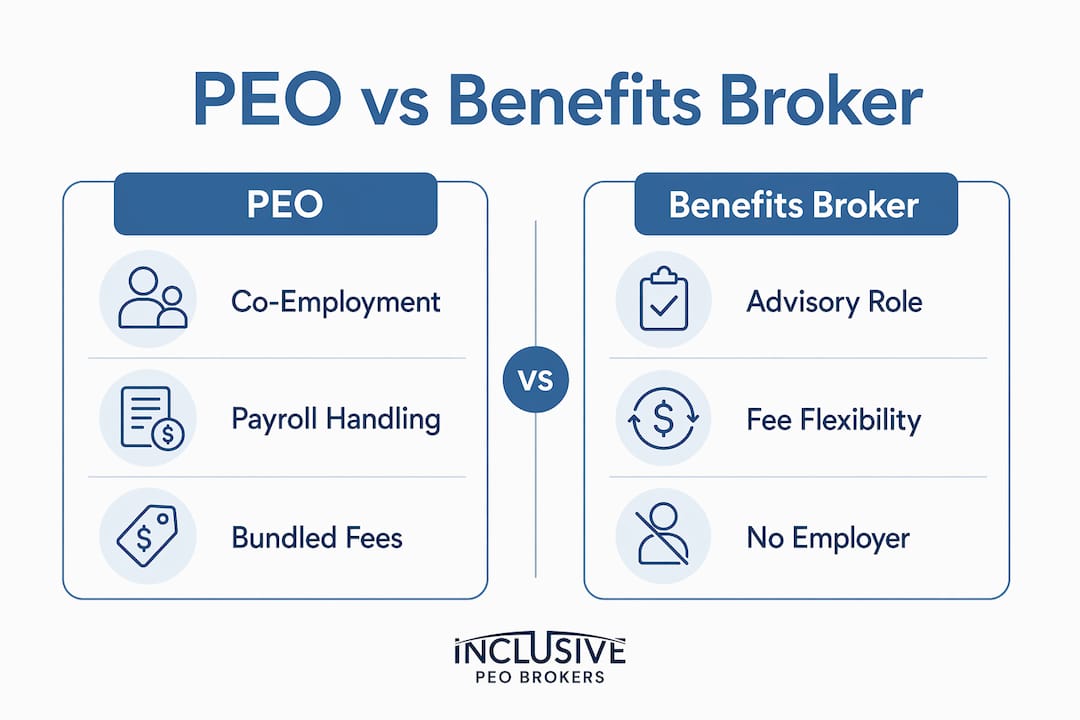

The fundamental structural difference between a PEO and a benefits broker is that a PEO becomes the employer of record through a co-employment model, while a benefits broker remains an advisor without employer status. That single distinction drives every other difference between the two.

Under co-employment, the PEO legally shares employer responsibilities with you. It handles payroll processing, tax filings, workers’ compensation, and benefits administration. You retain control over day-to-day operations and hiring decisions. A benefits broker, by contrast, shops the insurance market on your behalf, recommends plans, and supports enrollment. The broker does not touch your payroll or compliance obligations.

| Feature | PEO | Benefits Broker |

|---|---|---|

| Employer of record | Yes, co-employment | No |

| Payroll and tax filing | Included | Not included |

| Benefits administration | Bundled | Primary service |

| Carrier and vendor access | Limited to PEO network | Broad market access |

| Compliance support | Included | Limited or add-on |

| Contract commitment | Typically one year | Flexible, often annual |

| Pricing model | Per-employee fee or % of payroll | Commission or flat fee |

PEO contracts typically involve one-year commitments and bundled service fees, while brokers offer more flexible arrangements and earn through commissions or service fees. That pricing difference matters when you are budgeting for HR costs. A PEO fee is predictable but all-in. A broker’s compensation can be harder to trace unless you ask for full disclosure upfront.

Pro Tip: Ask any PEO or broker to provide a written breakdown of all fees before you sign anything. Bundled pricing is not the same as transparent pricing.

PEO vs. benefits broker: which fits your business size?

PEOs serve startups and very small teams best, while benefits brokers tend to deliver more value for growing businesses with 50 or more employees who want customization and control. This is not a hard rule, but it reflects how each model is built.

A PEO gives a five-person startup access to Fortune 500-level benefits by pooling employees across its entire client base. That scale produces lower insurance premiums and access to plans a tiny company could never negotiate alone. The tradeoff is limited flexibility. You choose from the PEO’s pre-negotiated plan menu, not the open market.

Once your headcount grows past 50 employees, a benefits broker often makes more sense. At that size, you have enough purchasing power to negotiate directly with carriers. A broker gives you access to the full market, lets you design custom plan structures, and helps you build a benefits strategy that reflects your company culture.

Key factors to weigh when deciding:

- Headcount and growth trajectory. Under 25 employees, a PEO’s pooled buying power is hard to beat. Above 50, a broker’s market access becomes more valuable.

- Desired control over plan design. PEOs offer limited customization. Brokers let you select carriers, deductibles, and network types independently.

- Internal HR capacity. If you have no HR staff, a PEO’s bundled administration fills that gap. A broker assumes you have someone managing HR internally.

- Compliance complexity. Multi-state employers or those in regulated industries often benefit from a PEO’s built-in compliance infrastructure.

- Long-term cost strategy. Brokers can pursue alternative funding models like level-funded or self-funded plans as you scale. PEOs rarely offer those options.

Pro Tip: If you are planning to hire aggressively in the next 12 months, model both options at your projected headcount, not your current one. The right choice today may not be the right choice at 75 employees.

How do you launch a benefits broker RFP?

A structured benefits broker RFP includes seven core sections: company overview, current benefits summary, broker team experience, service model, technology and data capabilities, fees and compensation, and references. Each section exists to create a consistent basis for comparison across multiple candidates.

The RFP process matters because it forces every broker to answer the same questions in the same format. Without it, you end up comparing a polished sales pitch from one firm against a detailed technical proposal from another. That comparison is meaningless. A controlled RFP process ensures transparency and consistency, which leads to better long-term partnerships aligned with your goals.

Here is a practical sequence to follow:

- Define your evaluation criteria. Decide which factors matter most: cost, compliance expertise, technology, or employee experience. Assign percentage weights to each category before you read a single proposal.

- Write the RFP document. Include your company size, current benefits spend, renewal date, and specific pain points. Be specific. Vague RFPs attract vague responses.

- Identify three to five broker candidates. Use referrals, industry associations, or a PEO broker matching service to build your shortlist.

- Send the RFP with a firm deadline. Give brokers two to three weeks to respond. A shorter window filters out firms that are not organized.

- Score responses against your weighted criteria. Use a simple scoring matrix. Rate each broker on strategy, service quality, cost model, and compliance approach.

- Conduct finalist interviews. Ask each finalist to walk through their fee model and describe how they handled a client’s renewal challenge.

- Check references. Call at least two current clients with similar company sizes and ask about issue resolution speed and year-over-year cost trends.

| RFP Section | What to Evaluate |

|---|---|

| Broker team experience | Years in market, industry specialization, client retention rate |

| Service model | Dedicated account manager, response time commitments |

| Technology and data | Benefits portal, reporting dashboards, enrollment tools |

| Fees and compensation | Commission vs. flat fee, total cost disclosure |

| References | Client size match, renewal performance, satisfaction scores |

Pro Tip: Weight fee transparency at no less than 20% of your total RFP score. Brokers who resist full disclosure during the proposal stage rarely improve after you sign.

How do you evaluate broker performance at renewal?

Renewal is the most revealing moment in any broker relationship. Evaluating brokers on year-over-year cost trends and operational KPIs uncovers whether they manage outcomes or merely process transactions. Most small businesses skip this evaluation entirely and simply accept whatever renewal package arrives.

The key performance indicators to request from your broker include:

- Cost trend vs. market benchmarks. Your renewal increase should be compared against industry averages for your region and company size.

- Employee satisfaction scores. Did your team actually use the benefits? Were there complaints about network access or claims support?

- Issue resolution speed. How quickly did the broker resolve billing errors, enrollment problems, or carrier disputes?

- Vendor and carrier adoption rates. Are employees using the plans as designed, or are they defaulting to the most expensive options?

“Ask your broker whether they explored high-performance networks this renewal cycle. High-performance networks deliver better care at lower overall cost by directing employees to top-performing providers. If your broker has never raised this option, that tells you something.”

Brokers who cannot transparently disclose fee models and KPIs often underperform in managing operational issues, despite competitive initial plan placement. If your broker deflects questions about compensation or cannot produce performance data, treat that as a red flag. A broker who manages outcomes will welcome the conversation.

Pro Tip: Schedule your renewal review 90 days before your contract end date, not 30. That window gives you time to run a competitive RFP if the conversation goes poorly.

Common mistakes in the PEO broker selection process

The peo broker selection process fails most often not because of bad options, but because of avoidable errors in how businesses approach the decision. Knowing these pitfalls in advance saves you from costly course corrections later.

The most frequent mistakes include:

- Accepting bundled PEO plans without asking for a cost breakdown. Bundled pricing is convenient, but it can hide markups on individual services. Always request a line-item breakdown before signing.

- Ignoring broker compensation disclosures. Demanding detailed compensation breakdowns and KPI disclosure tied to issue resolution is the single most effective way to identify brokers who will deliver ongoing value. Skipping this step is the most common and most expensive mistake.

- Failing to involve key stakeholders. HR managers should not make this decision alone. Finance, operations, and even a sample of employees should weigh in on benefits priorities before you select a partner.

- Choosing based on price alone. The lowest-cost broker or PEO is rarely the best long-term partner. A broker who saves you 5% on premiums but costs you 20 hours a year in administrative problems is not a bargain.

- Not planning for scalability. The right partner at 15 employees may not be equipped to serve you at 80. Ask every candidate how their service model changes as your headcount grows.

Key takeaways

The most effective way to choose between a PEO and a benefits broker is to match the model to your headcount, control needs, and internal HR capacity, then validate your choice through a structured RFP and annual performance review.

| Point | Details |

|---|---|

| PEO vs. broker structure | A PEO takes on co-employment status; a broker advises without employer responsibility. |

| Business size threshold | PEOs fit best under 25 employees; brokers add more value above 50 with custom plan design. |

| RFP process discipline | A seven-section RFP with weighted scoring produces objective, comparable broker proposals. |

| Renewal evaluation | Request cost trend data, KPIs, and fee disclosures at every renewal to hold brokers accountable. |

| Transparency as a filter | Brokers who resist disclosing compensation models are a reliable predictor of future service problems. |

What i have learned about choosing between peos and brokers

After working through dozens of PEO and broker evaluations with small business owners, the pattern I see most often is this: businesses choose based on what is familiar, not what fits. A founder who used a PEO at a previous company defaults to a PEO. An HR manager who came from a large company defaults to a broker. Neither instinct is wrong, but neither is a strategy.

The control-versus-convenience tradeoff is real. A PEO genuinely does offload administrative burden. But that convenience comes with reduced flexibility, and I have seen businesses outgrow their PEO arrangements and face painful transitions because they did not plan for it. Conversely, I have seen small teams without dedicated HR staff choose a broker and then struggle to manage compliance and enrollment on their own.

The businesses that get this right treat the selection process as a partnership decision, not a vendor purchase. They ask hard questions about fee structures, they involve their team in benefits design, and they set clear performance expectations before the contract is signed. The ones who struggle treat it as a checkbox exercise.

My honest advice: use a structured RFP even if you think you already know who you want to hire. The process itself reveals things that a sales conversation never will. And at renewal, do not accept a passive presentation. Ask your broker to defend their performance with data. If they cannot, you have your answer.

— John

How inclusive PEO brokers simplifies your selection process

Choosing between a PEO and a benefits broker is a significant decision, and most small business owners do not have 80 hours to spend researching options, issuing RFPs, and comparing proposals. That is exactly the problem Inclusive PEO Brokers was built to solve.

Inclusive PEO Brokers has completed 133 successful PEO implementations and saves clients an average of 80 hours in the selection process, with an average cost saving of $634. The process is built around your specific business needs, not a generic shortlist. Whether you are evaluating your first PEO selection or comparing your current arrangement against broker alternatives, Inclusive PEO Brokers provides the expert guidance to get you to the right answer faster. Visit Inclusive PEO Brokers to start a personalized consultation.

FAQ

What is the core difference between a PEO and a benefits broker?

A PEO enters a co-employment relationship with your business and handles payroll, compliance, and benefits administration. A benefits broker advises on plan selection and carrier options without taking on any employer status.

When does a PEO make more sense than a benefits broker?

PEOs are most effective for startups and businesses with fewer than 25 employees who need bundled HR support and access to group benefits they could not otherwise afford. Brokers become more valuable as headcount and purchasing power grow.

What should a benefits broker RFP include?

A strong RFP covers company overview, current benefits, broker team experience, service model, technology capabilities, fee and compensation structure, and client references. Consistent criteria across all candidates is what makes the comparison valid.

How do you know if your benefits broker is underperforming?

Request year-over-year cost trend data, employee satisfaction scores, and issue resolution metrics at every renewal. Brokers who cannot or will not provide this data are a strong indicator of a service problem.

Can a small business use both a PEO and a benefits broker?

In most cases, no. A PEO’s co-employment model includes benefits administration as part of its bundled service, which makes a separate benefits broker redundant. Some businesses transition from a PEO to a broker model as they scale and want more control over plan design.

Recommended

.svg)

Seeking a different solution? Meet Your Business Needs