.png)

Pet Insurance Employee Benefit: What HR Needs to Know

Pet insurance as an employee benefit is a voluntary workplace program where employers negotiate group-rate policies that employees pay for through payroll deductions, reducing the financial shock of unexpected veterinary costs. Formally classified under voluntary benefits, this offering costs employers little to nothing in direct premiums while delivering measurable value to pet-owning staff. The concept is straightforward: your organization partners with a carrier like MetLife Pet Insurance or Nationwide, secures discounted group rates, and employees opt in during open enrollment. With pet insurance adoption rising to 22% of organizations offering it in 2026, up from 14% in 2022, HR professionals who ignore this trend risk falling behind in a competitive talent market.

What is pet insurance as an employee benefit?

Pet insurance as an employee benefit is a voluntary, employee-paid program that gives workers access to group-rate pet health insurance policies administered through their employer. The employer does not typically fund the premiums. Instead, the employer’s role is mostly setup and administration, not premium funding. This distinction matters because many HR teams assume the benefit requires a budget line. It does not.

The mechanics mirror other voluntary benefits like supplemental life or disability insurance. Employees select a plan during open enrollment, choose their coverage tier, and premiums are deducted automatically from each paycheck. The reimbursement-based model is the most common structure in the U.S.: employees pay the vet bill at the time of service, then submit a claim to the carrier for reimbursement.

Does pet insurance count as a benefit? Yes. The IRS classifies it as a voluntary employee benefit, similar to accident insurance or legal services plans. It appears in the benefits package as an elective offering, and employees can typically enroll, change, or cancel coverage during designated windows.

How does pet insurance work as a voluntary employee benefit?

The operational flow has four steps: enrollment, payroll deduction, vet visit, and claim submission. Understanding each step helps both HR professionals and employees set accurate expectations before the first policy goes live.

Here is how the process works in practice:

- Enrollment: Employees opt in during open enrollment or a qualifying life event. They select a plan tier, deductible level, and reimbursement percentage.

- Payroll deduction: Premiums are automatically withheld before the employee receives their paycheck. Payroll deduction reduces coverage lapses by 15 to 25 percentage points compared to direct-to-consumer policies because it removes the friction of missed payments.

- Vet visit: The employee pays the full veterinary bill at the time of service. There is no insurance card to swipe at the front desk.

- Claim submission: The employee submits an itemized invoice to the carrier, either online or through a mobile app. Reimbursement follows after the deductible is applied.

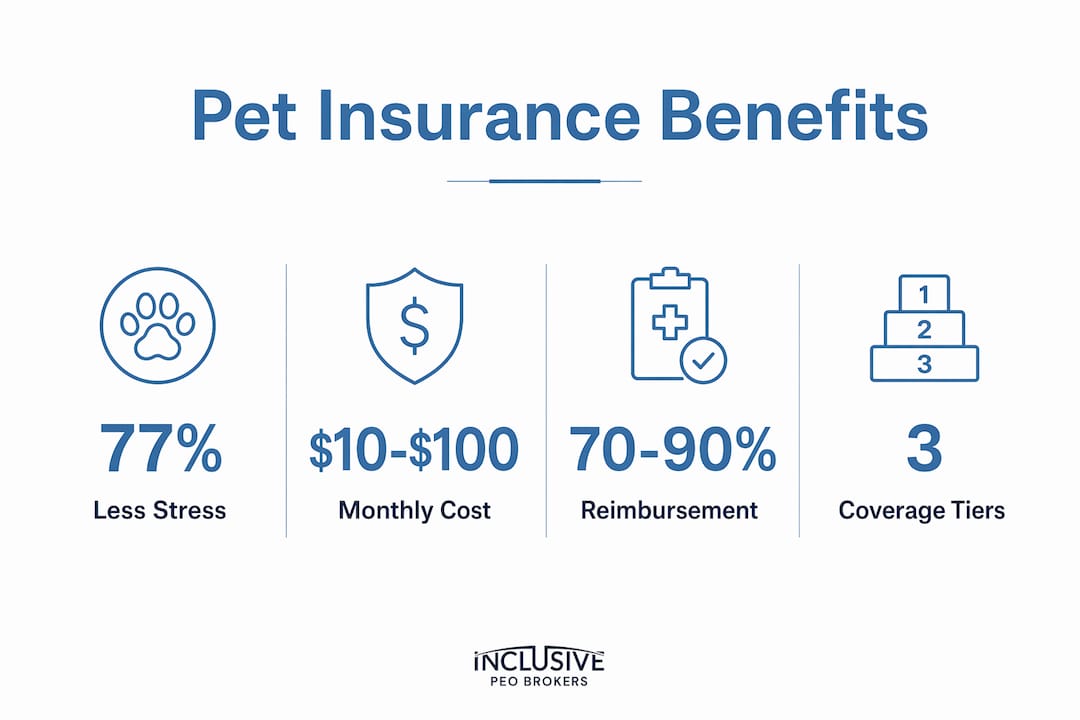

Common reimbursement percentages are 70%, 80%, or 90% after the deductible. A practical example: a $3,000 emergency surgery bill with a $500 deductible leaves $2,500 eligible for reimbursement. At 80%, the employee receives $2,000 back. That is a significant reduction in out-of-pocket exposure for a working pet owner.

Waiting periods and exclusions vary by carrier and plan. Accident coverage often activates within 0 to 3 days of enrollment, while illness coverage typically carries a 14-day waiting period. Pre-existing conditions are almost universally excluded. Communicating these details upfront prevents frustration and erodes trust in the benefit if employees discover them only after filing a claim.

Pro Tip: Include a one-page policy summary in your onboarding packet that clearly states waiting periods, exclusion categories, and the claims submission process. Employees who understand the mechanics from day one are far more likely to use the benefit and value it.

What coverage options come with employee benefits pet coverage?

Pet insurance plans offered through employer programs generally fall into three tiers. The right tier for your workforce depends on employee demographics, average pet age, and how much premium employees are willing to absorb.

| Plan Type | What It Covers | Typical Monthly Premium |

|---|---|---|

| Accident-only | Injuries from accidents (fractures, lacerations, ingestion of foreign objects) | $10 to $25 per pet |

| Accident and illness | Accidents plus diseases, infections, cancer, and hereditary conditions | $30 to $60 per pet |

| Comprehensive with wellness | All of the above plus routine care (vaccines, dental cleanings, annual exams) | $60 to $100+ per pet |

Pet insurance premiums range from $10 to over $100 per pet per month depending on plan type, species, pet age, and geographic region. A three-year-old mixed-breed dog in San Francisco will cost more to insure than the same dog in rural Ohio, simply because veterinary costs differ by market.

The accident and illness tier is the most popular choice among employees because it covers the scenarios most likely to generate a large, unexpected bill. Cancer treatment, for example, can exceed $10,000 for a dog. Accident-only plans are a lower-cost entry point but leave employees exposed to the most financially damaging claims.

Wellness add-ons appeal to employees who want to offset routine care costs. These riders typically reimburse a fixed annual amount for preventive services rather than operating on a percentage basis. They are worth including as an option, but HR should not position them as the primary selling point of the program.

Pro Tip: Offer at least two plan tiers during enrollment. Employees with young, healthy pets often choose accident-only coverage to keep premiums low, while those with older pets or specific breeds prone to hereditary conditions gravitate toward accident and illness plans. Giving employees a real choice increases participation rates.

Why offer pet insurance to employees? The case for HR and leadership

The strategic case for adding employee benefits pet coverage rests on three pillars: financial well-being, talent retention, and workplace culture.

Financial well-being: 77% of employees with pet insurance report worrying less about unexpected pet health expenses. Financial stress is a documented productivity drain. When employees are not mentally calculating how to cover a $4,000 vet bill, they are more present and focused at work. Pet insurance directly addresses a source of anxiety that traditional health or financial wellness programs do not touch.

Talent retention and recruitment: Over half of working pet parents have considered changing jobs for better pet benefits. That figure is not a rounding error. It reflects a genuine shift in how millennial and Gen Z workers evaluate total compensation. For HR professionals competing for talent in professional services, technology, or healthcare, pet insurance is a low-cost differentiator that resonates with a large segment of the workforce.

Workplace culture: Adding pet health insurance for workers signals that your organization recognizes the full context of employees’ lives. Pets are family members for most owners. A benefits package that acknowledges that reality communicates something meaningful about your company’s values.

“Pet insurance fits naturally into a total rewards strategy that treats employees as whole people, not just workers. It costs the employer almost nothing to offer, yet the perceived value to a pet-owning employee is substantial.” — Benefits advisory perspective aligned with Nationwide’s voluntary benefits research

The employer cost structure reinforces the case. Because premiums are employee-paid, your direct financial exposure is limited to administrative setup and payroll system configuration. The group rate discount your employees receive through the employer program is the primary value lever, not a subsidy from your budget.

How can HR implement pet insurance benefits effectively?

Adding pet insurance to your voluntary benefits package is a four-phase process: carrier selection, payroll integration, employee communication, and ongoing management.

-

Select a reputable carrier or platform. MetLife Pet Insurance, Nationwide, and Figo are among the established carriers offering employer group programs. Evaluate carriers on network breadth, claims processing speed, mobile app quality, and the flexibility of their plan designs. Ask for group rate schedules specific to your workforce’s zip code distribution.

-

Integrate with your existing payroll and benefits administration system. Adding pet insurance to existing benefit enrollment and payroll systems reduces administrative complexity significantly. Most carriers support EDI (electronic data interchange) feeds or work directly with platforms like Workday, ADP, or Paylocity. Confirm the reconciliation model upfront: some carriers handle individual reconciliation directly, while others accept aggregated employer remittances.

-

Educate employees on policy mechanics, not just emotional appeal. The most common source of dissatisfaction with pet insurance is unmet expectations. Employees who enroll without understanding waiting periods, deductibles, or exclusions often feel misled when a claim is denied. Use your employee benefits broker to create plain-language materials that explain exactly how the reimbursement process works, what is excluded, and how to file a claim.

-

Time enrollment strategically and communicate year-round. Open enrollment is the obvious window, but mid-year reminders, new-hire onboarding packets, and internal Slack or Teams posts keep the benefit visible. Employees who adopt a new pet mid-year often do not realize they may qualify for a special enrollment period. Proactive communication captures those moments.

-

Track participation and gather feedback. Measure enrollment rates by department and tenure. Low participation in a specific group often signals a communication gap rather than a lack of interest. Survey employees annually to understand whether the plan design still fits their needs.

Pro Tip: Partner with your PEO or benefits broker to negotiate group rates before your first open enrollment. Carriers offer better pricing when they can see workforce size and demographic data. A broker with experience in voluntary benefits strategies can often secure 5 to 15% lower premiums than employers negotiating directly.

Key takeaways

Pet insurance as an employee benefit is a low-cost, high-impact voluntary program that HR professionals can add to strengthen retention, reduce employee financial stress, and signal a people-first workplace culture.

| Point | Details |

|---|---|

| Employer cost is minimal | Premiums are employee-paid; employer role is setup and payroll administration only. |

| Payroll deduction drives retention | Automatic deduction reduces policy lapses by 15 to 25 percentage points versus direct billing. |

| Three coverage tiers exist | Accident-only, accident and illness, and comprehensive wellness plans serve different employee needs and budgets. |

| Adoption is accelerating | 22% of organizations offered pet insurance in 2026, up from 14% in 2022, signaling competitive pressure. |

| Communication is the critical variable | Clear education on waiting periods, exclusions, and claims process determines employee satisfaction with the benefit. |

Why I think HR teams are underselling this benefit

I have spent years watching HR professionals agonize over benefits budgets while overlooking programs that cost almost nothing to offer. Pet insurance is the clearest example of that pattern. The objection I hear most often is: “We do not have the budget.” That objection collapses the moment you realize the employer is not paying the premium. You are negotiating access and a group discount. The employee pays the rest.

What I find more interesting is the retention angle. The data point that over half of working pet parents have considered changing jobs for better pet benefits is not a soft, feel-good statistic. It is a direct signal about what a meaningful segment of your workforce values. If your competitors are offering pet insurance and you are not, you are losing candidates and potentially employees without ever knowing why.

The implementation concern is also overstated. Most modern payroll platforms handle voluntary benefit deductions without custom development. The carrier does the heavy lifting on reconciliation. Your HR team’s actual workload is a few hours of setup and an annual communication push.

The one area where I think employers genuinely underinvest is employee education. Enrolling employees in a benefit they do not understand creates more dissatisfaction than not offering it at all. The fix is simple: plain-language materials, a short FAQ, and a clear explanation of what the benefit does not cover. That investment pays for itself the first time an employee files a successful claim and tells a colleague about it.

Pet insurance is not a luxury add-on for large enterprises. It is a practical, low-overhead voluntary benefit that fits the total rewards strategy of any organization with a workforce that includes pet owners. Given workforce demographics, that is most organizations.

— John

How Inclusive PEO Brokers can help you add pet insurance to your benefits package

Adding pet insurance to your voluntary benefits lineup is straightforward when you have the right infrastructure in place. Inclusive PEO Brokers works with small and medium-sized businesses to identify PEO partners that include group-rate pet insurance plans, payroll deduction integration, and full benefits administration support.

Through Inclusive PEO Brokers’ PEO matching process, your organization gains access to carriers and plan designs that would otherwise require direct negotiation. Clients save an average of 80 hours in the selection process and $634 in administrative costs, with 133 successful implementations completed to date. If you are ready to build a benefits package that retains talent and reduces HR complexity, start with Inclusive PEO Brokers to find the right fit for your workforce.

FAQ

What is a pet insurance employee benefit?

A pet insurance employee benefit is a voluntary program where employers provide employees access to group-rate pet insurance policies, with premiums paid by employees through payroll deduction. The employer typically pays no direct premium cost.

Does pet insurance count as an employee benefit?

Yes. Pet insurance is classified as a voluntary employee benefit, similar to supplemental life or accident insurance. It appears in the total rewards package as an elective offering employees can enroll in during open enrollment.

Why offer pet insurance to employees?

Pet insurance reduces financial stress for pet-owning employees, with 77% reporting less worry about unexpected vet costs. It also strengthens recruitment and retention, particularly among millennial and Gen Z workers.

How much does pet insurance cost as an employee benefit?

Premiums range from $10 to over $100 per pet per month depending on plan type, pet species, age, and location. Employers pay little to no direct cost since premiums are employee-funded through payroll deduction.

What coverage do employee pet insurance plans typically include?

Most employer programs offer three tiers: accident-only, accident and illness, and comprehensive plans with wellness add-ons. Reimbursement rates of 70%, 80%, or 90% apply after the employee meets their chosen deductible.

Recommended

.svg)

Seeking a different solution? Meet Your Business Needs