.png)

The Role of Benefits Administration in PEO Partnerships

Every benefits administration error costs your business an average of $500 per incident. Multiply that across open enrollment season, new hire onboarding, and qualifying life events, and the financial exposure adds up fast. For HR professionals and business owners managing benefits independently, the complexity is real: multiple vendors, disconnected systems, compliance deadlines, and employees who expect answers immediately. The role of benefits administration in PEO partnerships addresses exactly this problem. A Professional Employer Organization takes on co-employment responsibilities, including the full operational weight of managing your benefits programs, so your team can focus on work that actually grows the business.

Table of Contents

- Key Takeaways

- The role of benefits administration in PEO structures

- How PEOs use technology to improve benefits management

- Business outcomes driven by PEO benefits administration

- In-house benefits management vs. PEO administration

- My take on benefits administration as a strategic tool

- How Inclusive PEO Brokers can help you get this right

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| PEOs handle end-to-end benefits admin | From enrollment to compliance, PEOs manage the full benefits administration lifecycle under a co-employment model. |

| Integrated tech reduces errors significantly | Platforms connecting payroll, HRIS, and benefits carriers cut enrollment processing time by 40 to 60 percent. |

| Small businesses access Fortune 500 benefits | PEO benefits pooling gives smaller employers access to health plans and rates typically reserved for large corporations. |

| Benefits admin drives retention and growth | Effective benefits communication and administration directly improve employee satisfaction and reduce costly turnover. |

| Expert brokers reduce transition risk | Specialized PEO brokers negotiate better terms and prevent coverage gaps when switching or exiting PEO arrangements. |

The role of benefits administration in PEO structures

When you partner with a PEO, you enter a co-employment arrangement. The PEO becomes the employer of record for tax and benefits purposes, while you retain full control over day-to-day operations and management decisions. Within that structure, benefits administration functions cover four core areas: enrollment, eligibility management, employee communication, and regulatory compliance.

Here is what PEO benefits management looks like in practice:

- Enrollment management. The PEO handles open enrollment, new hire benefit elections, and qualifying life event changes such as marriage, birth, or loss of other coverage. This removes the back-and-forth between your HR team, employees, and carriers.

- Eligibility verification. The PEO continuously tracks which employees qualify for which plans based on hours worked, employment status, and waiting periods. Manual tracking of this data is where most in-house errors originate.

- Carrier coordination and claims support. Your PEO manages the relationship with health, dental, vision, life, and disability carriers. When an employee has a claims issue, the PEO’s benefits team is the first point of contact.

- Payroll integration and deductions. Benefits deductions sync directly with payroll processing, which eliminates duplicate data entry and reduces the risk of under-deducting or over-deducting employee premiums.

- Regulatory compliance. This includes COBRA administration, Affordable Care Act reporting, Section 125 plan management, and annual filings. These are areas where non-compliance penalties can far exceed the cost of outsourcing.

- Employee communication. PEOs provide benefits guides, decision-support tools, and direct employee support during enrollment periods, which increases plan participation and reduces confusion.

The combined effect of these responsibilities is a significant reduction in your administrative burden. Poor system integration is the leading cause of benefits errors, and a PEO’s centralized approach directly addresses that root cause.

Pro Tip: When evaluating a PEO, ask specifically how they handle qualifying life event changes outside of open enrollment. The speed and accuracy of mid-year updates is one of the clearest indicators of how well their benefits administration actually functions.

How PEOs use technology to improve benefits management

The efficiency gains from PEO benefits management are not accidental. They come from purpose-built technology that connects systems which are typically siloed in independent businesses.

Here is how the technology integration typically works:

- Unified data entry. Employee information entered during onboarding flows automatically into payroll, benefits enrollment, and HRIS records. You enter data once instead of three times across three platforms.

- Automated eligibility updates. When an employee’s status changes, such as moving from part-time to full-time, the system flags the benefits eligibility change and routes it for action without requiring manual intervention.

- COBRA and ACA automation. Notifications, election periods, and required reporting are triggered automatically based on employment events, which removes the risk of missed deadlines.

- Centralized reporting dashboards. HR teams and business owners get real-time visibility into benefits participation, costs by plan, and upcoming renewal dates, all in one place.

- Carrier invoicing reconciliation. The PEO’s platform matches carrier invoices against actual enrollment data each month, catching billing discrepancies before they become overpayments.

Integrated benefits platforms reduce enrollment processing time by 40 to 60 percent compared to organizations using disconnected point solutions. That is not a marginal improvement. For a 50-person company processing annual enrollment, that difference can represent dozens of hours reclaimed for your HR team.

| Approach | Enrollment Processing Time | Error Rate | Compliance Risk |

|---|---|---|---|

| Standalone, disconnected systems | High (manual, multi-step) | Elevated | High without dedicated staff |

| PEO with integrated platform | Reduced by 40 to 60% | Significantly lower | Managed by PEO compliance team |

HR automation also drives higher participation rates, because employees who find enrollment easy are more likely to complete it accurately and on time. That matters for your benefits spend and for employee satisfaction scores.

Pro Tip: Ask any PEO you are evaluating to show you a live demo of their benefits administration portal. Pay attention to how many clicks it takes an employee to complete enrollment. Friction in the employee experience translates directly into HR support tickets and errors.

Business outcomes driven by PEO benefits administration

The importance of benefits administration extends well beyond operational efficiency. When a PEO manages your benefits program effectively, the downstream effects touch cost, compliance, retention, and your ability to compete for talent.

Access to better benefits at lower cost

PEOs enable small businesses to offer Fortune 500-level benefits by pooling employees across their entire client base. This is the role of benefits pooling in PEO arrangements. A 20-person company on its own cannot negotiate competitive group health rates. That same company under a PEO’s master plan gains access to carrier relationships built on thousands of covered lives, which translates to better plan options and more favorable pricing.

The numbers can be striking. In one documented case, a 97-employee company working with a PEO broker saved $399,484 annually while securing a 15-month rate guarantee and $3 million in EPLI coverage. That outcome was not the result of luck. It came from expert negotiation and a broker who understood how to structure the deal.

Compliance protection and reduced liability

Benefits compliance is one of the most consequential areas of HR risk for small and mid-size businesses. ACA reporting errors, missed COBRA deadlines, and Section 125 plan violations carry penalties that can reach tens of thousands of dollars. Under a co-employment model, the PEO shares compliance responsibility, which means their legal and compliance teams are actively monitoring regulatory changes and updating your plan administration accordingly.

“Benefits administration has evolved from a routine back-office function into a critical growth lever for organizations, impacting staffing stability and replacement costs.” — Economics of Growth in Employee Benefits Administration

Retention and talent acquisition

Employees who understand and value their benefits are more likely to stay. The importance of benefits in PEO partnerships is not just about cost savings. It is about the quality of the employee experience. When benefits communication is clear, enrollment is easy, and claims issues get resolved quickly, employees notice. That experience contributes directly to retention, which matters because replacing an employee typically costs between 50 and 200 percent of their annual salary.

You can see this dynamic play out in real client results where businesses that moved to a PEO reported measurable improvements in both benefits utilization and employee satisfaction scores within the first year.

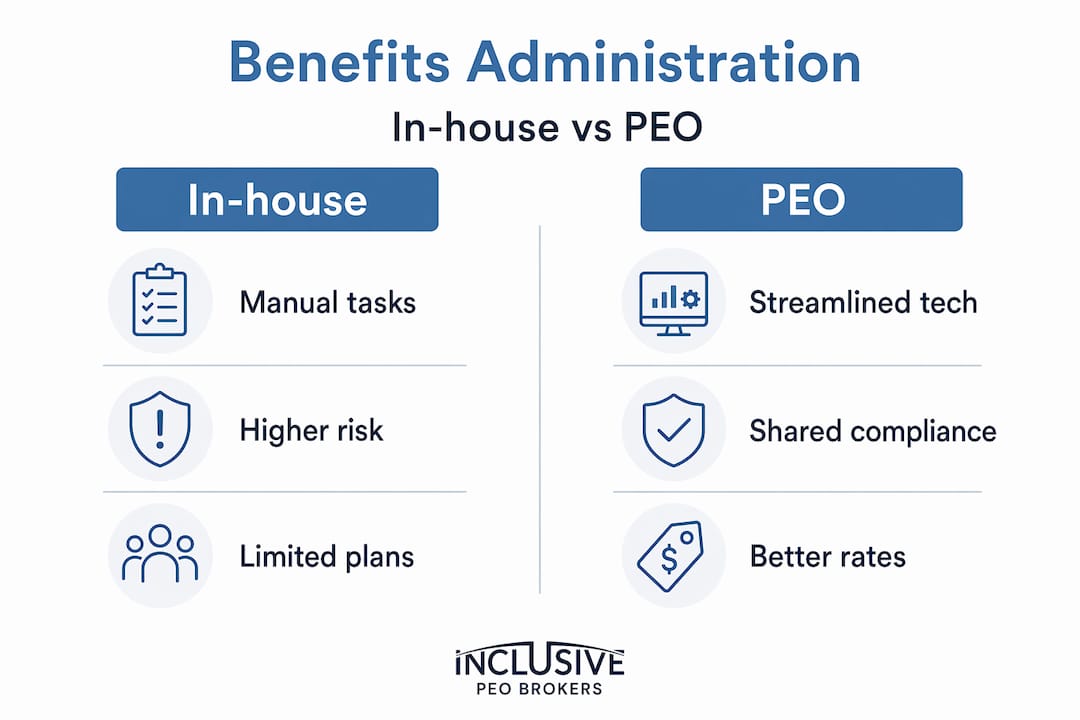

In-house benefits management vs. PEO administration

Managing benefits independently is not impossible. But the challenges compound quickly as your workforce grows or your benefits package becomes more complex.

Common pain points for businesses managing benefits without a PEO include:

- Vendor fragmentation. Health, dental, vision, life, disability, and FSA plans often sit with different carriers and require separate logins, invoices, and renewal timelines.

- Data silos. When payroll, HRIS, and benefits platforms do not talk to each other, disjointed point solutions create manual reconciliation work and increase the chance of costly errors.

- Compliance gaps. Without a dedicated compliance team, it is easy to miss regulatory updates. ACA reporting thresholds, COBRA election windows, and state-specific mandates change regularly.

- Limited plan options. Small employers negotiating directly with carriers have less leverage and fewer plan choices than businesses covered under a PEO’s master plan.

- Transition risks. Moving to or from a PEO without expert guidance can trigger payroll tax restarts, coverage gaps, and administrative disruptions. PEO transitions are typically completed in two to four weeks without coverage gaps when managed properly, but only when a knowledgeable broker is guiding the process.

The flip side is worth acknowledging. Some businesses that have been with a PEO for years find that bundled benefits packages limit their flexibility or that they have outgrown the arrangement. In those cases, the right move may be to explore exit options with a broker who can protect your employees’ coverage continuity during the transition.

Pro Tip: Before assuming your PEO’s benefits package is the best available, have an independent broker benchmark it against the open market annually. PEO benefits management benefits from outside perspective, especially at renewal time.

My take on benefits administration as a strategic tool

I have worked with dozens of businesses evaluating PEO partnerships, and the pattern I see most often is this: companies come in focused on cost and leave realizing that automated benefits administration is the part that actually changes how their HR team operates day to day.

What most employers overlook is the difference between offloading routine administration and building a strategic benefits program. A PEO can handle the former by default. The latter requires intentional plan design, data-informed decision making, and someone who understands both your workforce and the market. That is where a dedicated broker adds value that the PEO alone cannot provide.

I have also seen businesses stay in PEO arrangements long past the point where they made sense, simply because the transition felt too risky to manage. The reality is that PEO broker involvement eliminates most of that risk. The hidden costs of staying in the wrong arrangement, whether that means overpaying on premiums or accepting a benefits package that does not match your workforce’s needs, are almost always higher than the cost of making a well-managed change.

My honest advice: treat your benefits administration setup as workforce infrastructure, not a back-office task. The businesses that get this right attract better candidates, retain employees longer, and spend less time in reactive HR mode.

— John

How Inclusive PEO Brokers can help you get this right

If reading this article has you questioning whether your current benefits setup is working as hard as it should, that instinct is worth following.

Inclusive PEO Brokers specializes in matching small and mid-size businesses with PEOs that fit their specific workforce, industry, and benefits goals. The team has completed 133 successful implementations and saves clients an average of 80 hours in the selection process. Whether you are evaluating a PEO for the first time, benchmarking your current arrangement, or planning a transition, Inclusive PEO Brokers provides the expert guidance to get you to the right outcome. Explore your options with PEO services for small businesses or connect directly with a PEO broker in San Francisco to start the conversation.

FAQ

What is the role of benefits administration in a PEO?

Benefits administration in a PEO covers enrollment management, eligibility verification, carrier coordination, payroll deductions, compliance reporting, and employee communication. The PEO handles these functions under a co-employment model, reducing your administrative burden and compliance risk.

How does a PEO manage employee benefits?

A PEO manages employee benefits through integrated platforms that connect payroll, HRIS, and insurance carriers. This continuous monitoring approach automates routine tasks, reduces errors, and gives HR teams real-time visibility into plan participation and costs.

What is benefits pooling in a PEO?

Benefits pooling means the PEO combines employees from all its client companies into a single large group for insurance purchasing purposes. This gives small businesses access to better plan options and lower rates than they could negotiate independently.

Can a PEO help with benefits compliance?

Yes. PEOs share compliance responsibility under the co-employment arrangement, actively managing ACA reporting, COBRA administration, and Section 125 plan requirements. This significantly reduces the risk of penalties from missed deadlines or regulatory changes.

When should a business consider leaving a PEO?

A business should consider leaving a PEO when the bundled benefits package no longer fits its workforce needs, when costs exceed open-market alternatives, or when greater plan design flexibility is needed. Working with a broker to manage the transition protects employees from coverage gaps and prevents payroll tax disruptions.

Recommended

.svg)

Seeking a different solution? Meet Your Business Needs