.png)

Upgrade Your Employee Benefits Package: 2026 Guide

An employee benefits package upgrade is the structured process of evaluating, redesigning, and communicating your total rewards offering to better meet workforce needs, regulatory requirements, and business goals. For small to medium-sized businesses, getting this right in 2026 means more than adding a gym stipend. It means building a package that competes with larger employers on health coverage, financial wellness, and flexibility. Research shows 85% of organizations report that benefits directly improve employee satisfaction and retention. That number tells you this is not a nice-to-have. It is your most underused retention tool.

How to upgrade your employee benefits package step by step

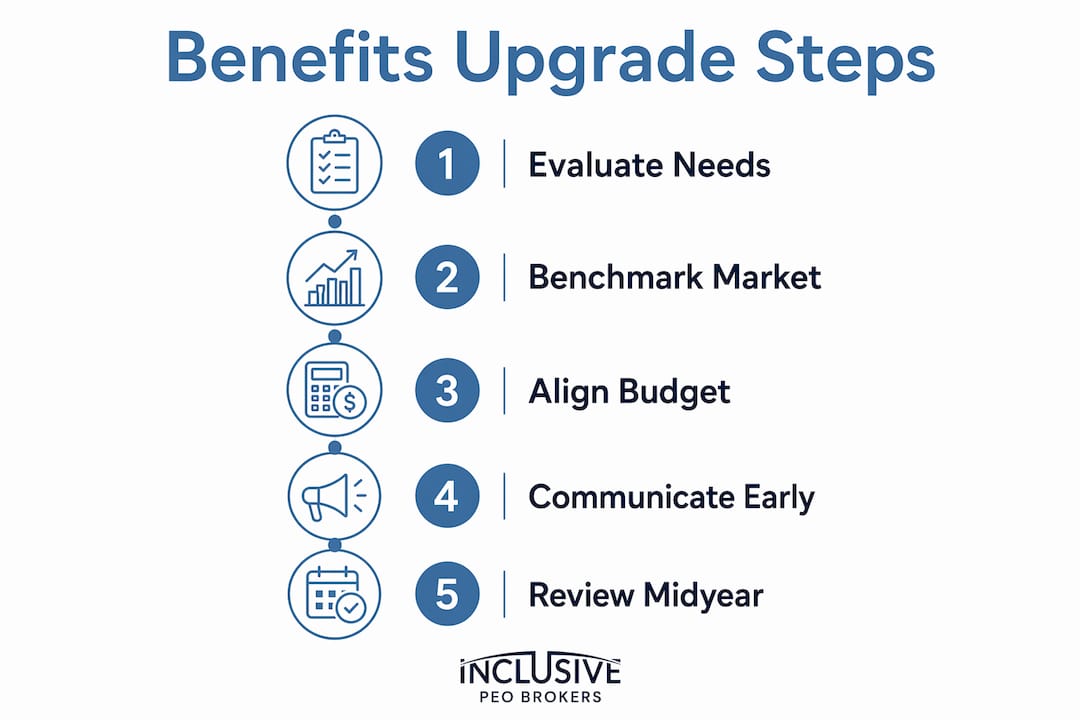

The industry term for this process is total rewards redesign, and it follows a clear sequence. Oyster’s four-step benefits design framework gives SMBs a practical starting point: evaluate workforce needs, benchmark competitors, align your budget, and communicate clearly. Each step builds on the last, and skipping one creates gaps that show up during open enrollment or, worse, in your turnover numbers.

Step 1: Evaluate what your workforce actually needs. Run anonymous surveys and segment results by age, role, and family status. A 28-year-old software engineer and a 45-year-old warehouse supervisor have different priorities. One may want student loan repayment assistance; the other may prioritize dependent care FSAs. Consulting a benefits specialist at this stage prevents you from designing a package based on assumptions.

Step 2: Benchmark your current offering against the market. Pull data from industry salary surveys, the Bureau of Labor Statistics Employer Costs for Employee Compensation report, and your own employee benefits broker to understand where you stand. If your competitors offer HSA-qualified high-deductible health plans and you do not, that gap costs you candidates before they even reach the offer stage.

Step 3: Align your budget with 2026 IRS contribution limits. The IRS sets annual maximums for HSAs, retirement plans, and flexible spending accounts. These numbers define the ceiling for tax-advantaged employer contributions and must be factored into your plan design before you finalize costs.

Step 4: Build a communication strategy that starts early. Benefits communication should begin during recruiting, not at open enrollment. Candidates who understand your package before they accept an offer are more likely to stay long enough to use it.

Step 5: Schedule a mid-year review. A mid-year benefits review lets you assess cost trajectory, utilization patterns, and voluntary benefit enrollment before the next open enrollment cycle. This is where you catch underperforming plans and fix them without waiting a full year.

Pro Tip: Survey your employees before you redesign anything. The most common mistake SMBs make is adding benefits their workforce does not value, then wondering why satisfaction scores do not move.

How do 2026 IRS regulations affect health benefits design?

The 2026 IRS updates are not administrative trivia. They are design parameters that define what you can offer on a tax-advantaged basis. The IRS set the HSA maximum contribution at $4,400 for self-only coverage and $8,750 for family coverage. That means an employer pairing an HSA with a high-deductible health plan can contribute up to those amounts on a pre-tax basis, which is a meaningful compensation advantage for cost-conscious SMBs.

Healthcare cost growth of 8 to 10 percent in employer-sponsored plans is forcing a rethink of traditional plan design. Self-funded plans, level-funded arrangements, and reference-based pricing are no longer tools reserved for large corporations. SMBs with 50 or more employees are increasingly using these structures to control costs while maintaining competitive coverage.

The table below summarizes the key 2026 IRS thresholds that affect your plan design decisions:

| Benefit type | 2026 limit | Design implication |

|---|---|---|

| HSA (self-only) | $4,400 | Pairs with HDHP; employer can contribute pre-tax |

| HSA (family) | $8,750 | Higher employer contribution ceiling for family plans |

| HDHP minimum deductible (self) | $1,650 | Sets the floor for qualifying high-deductible plans |

| HDHP out-of-pocket max (family) | $16,600 | Caps employee exposure in qualifying plans |

Individual Coverage Health Reimbursement Arrangements, known as ICHRAs, are gaining traction as a defined-contribution alternative to group health plans. Under an ICHRA, you reimburse employees a fixed monthly amount to purchase their own individual coverage. This shifts plan selection to the employee and gives you predictable costs. However, ICHRA adoption significantly increases HR workload and requires dedicated benefits coordinators to handle employee questions and change management. Plan for that operational cost before you commit.

Pro Tip: Treat IRS limits as design inputs, not afterthoughts. Build your employer contribution strategy around the HSA and HDHP thresholds first, then layer in supplemental benefits. This prevents misaligned employee expectations and compliance issues down the line.

What modern benefits should you prioritize beyond health coverage?

Health insurance is the foundation, but it is no longer the differentiator. The benefits that separate competitive SMB packages from average ones in 2026 fall into four categories: financial wellness, voluntary supplemental coverage, mental health support, and flexible lifestyle benefits.

-

Financial wellness programs. According to Ascensus, 77% of organizations have or plan to implement financial wellness programs, driven largely by Millennial and Gen Z workforce expectations. These programs include retirement readiness education, budgeting tools, student loan repayment assistance, and emergency savings accounts. Earned wage access, which lets employees draw a portion of earned pay before payday, is also growing rapidly as a low-cost retention tool.

-

Voluntary supplemental health benefits. Accident insurance, critical illness coverage, and hospital indemnity plans allow employees to customize their protection beyond the base health plan. Only 11% of employers currently offer all three of these supplemental products, which means adding even one of them puts your package ahead of the majority. The EBRI data shows these voluntary offerings reduce absenteeism and improve morale in measurable ways.

-

Mental health support. Employee Assistance Programs are the baseline, but the workforce expects more. Integrated mental health platforms like Lyra Health or Spring Health provide therapy access, coaching, and crisis support through a single digital interface. Offering these signals that your company takes wellbeing seriously, which matters to candidates evaluating culture fit.

-

Lifestyle spending accounts and flexibility benefits. Lifestyle Spending Accounts, or LSAs, give employees a defined annual budget to spend on approved wellness categories: fitness, childcare, professional development, or home office equipment. Unlike FSAs, LSAs are post-tax and highly flexible. Paired with remote or hybrid work options, they signal trust and autonomy, two factors that consistently rank high in employee engagement surveys.

How can you optimize benefits communication and administration?

A generous package that employees do not understand is a wasted investment. Aon’s research confirms that tailored communication by employee demographics and preferences directly increases benefit utilization and satisfaction. The practical implication: one email blast during open enrollment is not a communication strategy.

Effective benefits communication for a multigenerational workforce requires multiple channels running simultaneously. Baby Boomers often prefer printed guides and one-on-one counseling sessions. Millennials and Gen Z respond to self-service digital platforms, short explainer videos, and mobile-first enrollment tools. Running both in parallel is not redundant. It is how you reach your full workforce.

-

Use a benefits administration platform. Tools like Rippling, Gusto, or BambooHR centralize enrollment, track utilization, and send automated reminders. These platforms reduce HR administrative time and give employees a single place to compare and elect options. The enrollment experience itself matters: a well-designed digital interface converts passive employees into active, informed participants.

-

Assign a benefits coordinator for complex plans. If you are implementing an ICHRA or a self-funded health plan, a dedicated coordinator is not optional. The administrative complexity of these plans generates a high volume of employee questions that your HR generalist cannot absorb alongside their regular workload.

-

Create a continuous feedback loop. Post-enrollment surveys, utilization reports, and manager check-ins give you real data on what is working. Use this data to inform your mid-year review and your next plan design cycle.

-

Start open enrollment communication six weeks early. Most employees make benefits decisions in the last 48 hours of the enrollment window. Starting earlier gives you time to educate, answer questions, and correct misconceptions before the deadline pressure hits.

Pro Tip: If you are managing benefits for a workforce with multiple generations, map your communication channels to each demographic before you write a single word of copy. Sending a PDF guide to a 24-year-old and a Slack message to a 58-year-old produces the opposite of the result you want.

You can also explore how other SMBs have handled benefit management challenges to see what communication and administration approaches translate across industries.

Key takeaways

A successful employee benefits package upgrade requires aligning 2026 IRS limits, workforce needs, and communication strategy before open enrollment begins.

| Point | Details |

|---|---|

| Start with workforce data | Survey employees by age and role before redesigning any benefit. |

| Use IRS limits as design inputs | Build HSA and HDHP contributions around 2026 thresholds to maximize tax advantage. |

| Add voluntary benefits strategically | Only 11% of employers offer all three supplemental health products; adding one differentiates your package. |

| Communicate across channels | Match communication format to employee demographics to improve utilization. |

| Review mid-year, not just annually | A mid-year check catches cost and enrollment issues before they compound. |

Why most SMBs get benefits upgrades wrong

After working with dozens of small and medium-sized businesses on HR strategy, the pattern I see most often is this: a company decides to upgrade its benefits package in September, tries to implement changes by November, and ends up with a rushed open enrollment that confuses employees and frustrates HR. The timeline is the first thing that breaks.

The second mistake is treating the upgrade as a one-time project rather than an ongoing process. Benefits strategy is not a set-it-and-forget-it function. Workforce expectations shift, IRS limits change, and healthcare costs move every year. The companies that retain their best people are the ones that treat benefits as a living program with regular review cycles built in.

I also want to be direct about ICHRAs. They are genuinely useful for certain SMBs, particularly those with geographically dispersed workforces where a single group plan cannot serve everyone well. But I have seen too many companies adopt ICHRAs because they sound modern, without accounting for the operational lift. If you do not have a dedicated benefits coordinator and a clear employee education plan in place before you launch, you will spend the first six months fielding confused calls instead of running your business.

The best benefits upgrades I have seen share one trait: they start with honest data about what employees actually value, not what leadership assumes they value. That distinction, between assumption and evidence, is where most packages succeed or fail.

— John

How Inclusive PEO Brokers helps SMBs upgrade their benefits

Upgrading your benefits package is a significant undertaking, and the administrative complexity grows quickly once you move beyond standard group health plans. Inclusive PEO Brokers specializes in matching small and medium-sized businesses with Professional Employer Organizations that handle benefits design, compliance, and administration as part of a co-employment model.

Inclusive PEO Brokers has completed 133 successful PEO implementations, saving clients an average of 80 hours in the selection process and $634 in costs. If you are ready to build a benefits package that competes with larger employers without adding headcount to your HR team, explore PEO services designed specifically for SMBs. The right PEO partner handles the complexity so you can focus on growth.

FAQ

What does upgrading an employee benefits package involve?

Upgrading a benefits package means evaluating current offerings, benchmarking against competitors, aligning plan design with IRS contribution limits, and improving how benefits are communicated and administered. The goal is a package that improves retention, attracts talent, and stays within budget.

What are the 2026 HSA contribution limits for employers?

The IRS set the 2026 HSA maximum at $4,400 for self-only coverage and $8,750 for family coverage. Employers can contribute up to these amounts on a pre-tax basis when pairing an HSA with a qualifying high-deductible health plan.

How do voluntary benefits improve employee retention?

According to EBRI, 85% of organizations report that voluntary benefits improve employee satisfaction and retention. Products like accident insurance, critical illness coverage, and hospital indemnity plans let employees customize their protection, which increases perceived value of the total package.

What is an ICHRA and is it right for small businesses?

An Individual Coverage Health Reimbursement Arrangement (ICHRA) lets employers reimburse employees a fixed amount to purchase individual health coverage. It offers cost predictability but increases HR workload significantly, requiring dedicated coordinator support and a clear employee education plan before launch.

How often should a small business review its benefits package?

At minimum, conduct a full review annually before open enrollment and a focused mid-year review to assess cost trajectory and utilization. Mid-year reviews allow you to adjust voluntary benefit offerings and correct enrollment issues before they carry into the next plan year.

Recommended

.svg)

Seeking a different solution? Meet Your Business Needs