.png)

Why a PEO Improves Benefits Access for Small Businesses

Small businesses rarely lose talent to bigger competitors because of salary alone. More often, the gap comes down to benefits. If you’ve ever tried to offer health insurance, a 401(k), or dental coverage as a small employer, you already know how expensive and administratively exhausting that process gets. Understanding why a PEO improves benefits access changes how you think about this problem entirely. A Professional Employer Organization pools your employees with thousands of others, giving you access to the same quality plans that Fortune 500 companies offer. This article breaks down exactly how that works, with the data to back it up.

Table of Contents

- Key Takeaways

- Why PEO improves benefits access through collective buying power

- Administrative and compliance advantages of PEO services

- How PEO-managed benefits affect retention and growth

- How to select a PEO that maximizes benefits access

- Common misconceptions about PEOs and benefits control

- My honest take on PEO benefits after years in this space

- How Inclusive PEO Brokers helps you find the right fit

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Collective buying power | PEOs pool employees across many businesses to negotiate group rates that individual SMBs cannot access alone. |

| Lower voluntary turnover | Businesses using PEO-managed benefits see 10-14% lower turnover within 18 months of adoption. |

| Reduced admin burden | PEOs handle enrollment, compliance reporting, and claims support so your HR team can focus on people, not paperwork. |

| Financial ROI is real | PEO clients save an average of $1,775 per employee yearly, with a 27% return on investment. |

| Selecting the right PEO matters | Verifying NAPEO membership and evaluating benefits customization options are the two most important steps in the selection process. |

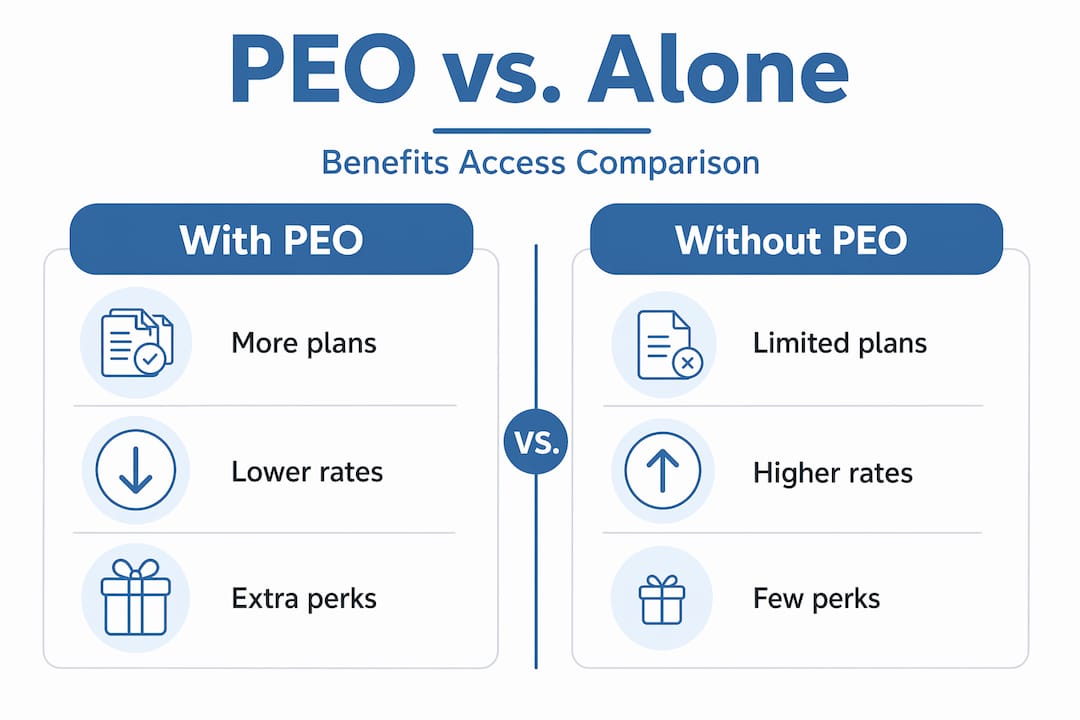

Why PEO improves benefits access through collective buying power

The core mechanic behind a PEO is the co-employment model. When you join a PEO, your employees are co-employed by both your company and the PEO. This is not a legal transfer of control. You keep full authority over hiring, firing, culture, and day-to-day operations. What changes is how your workforce is counted when it comes to insurance and benefits purchasing.

A PEO aggregates employees from dozens or hundreds of client companies into a single large group. That combined headcount, sometimes in the tens of thousands, gives the PEO significant negotiating leverage with insurance carriers. As a result, small businesses gain access to large-group health insurance plans even if they have as few as 10 employees. Without the PEO, those same companies would be purchasing individual small-group plans at significantly higher per-person rates.

The pricing difference is not trivial. PEO-negotiated rates with insurance providers typically run 15 to 25% lower than what a small business would pay on its own. Beyond cost, the plans themselves are broader. You get access to medical, dental, vision, life insurance, disability coverage, and retirement plans that would simply be out of reach or financially impractical to offer independently.

Here is a practical comparison of what this looks like for a 20-person company:

| Benefits Category | Without a PEO | With a PEO |

|---|---|---|

| Health insurance plan type | Small-group, limited carriers | Large-group, multiple tiers |

| Monthly premium per employee | $650 to $900 | $480 to $680 |

| 401(k) plan access | Basic or unavailable | Full plan with employer match options |

| Dental and vision | Often separate or dropped | Bundled, low-cost |

| Compliance management | DIY or costly consultants | Included in PEO service |

Pro Tip: When comparing PEO pricing, always ask for a total cost illustration that includes benefits savings, not just the PEO service fee. Many businesses find the benefits savings alone offset the cost of the PEO entirely.

Administrative and compliance advantages of PEO services

Buying power is only part of the story. The administrative and compliance support a PEO provides is where the real day-to-day relief comes from, especially for HR managers who are juggling too many responsibilities at once.

A PEO takes over benefits enrollment, handles employee questions about coverage, manages claims support, and submits all required regulatory filings. That includes ACA reporting, ERISA compliance, and Section 125 pre-tax plan administration. Section 125 plans allow employees to pay their benefit premiums with pre-tax dollars, which reduces both employee and employer payroll tax obligations. That is a meaningful cost reduction that many small businesses miss when managing benefits on their own.

The technology side matters too. PEOs reduce HR burden through digital platforms that give employees self-service access to their benefits, decision-support tools during open enrollment, and year-round educational resources. When employees actually understand their benefits, they use them more effectively and report higher satisfaction. Post-enrollment regret, where someone picks the wrong plan and resents it all year, drops significantly.

Here is what a well-structured PEO typically handles on the administrative side:

- Benefits enrollment and mid-year life-event changes

- COBRA administration when employees leave

- ACA compliance, including 1094/1095 reporting

- Workers’ compensation policy management

- ERISA documentation and plan filings

- Section 125 cafeteria plan setup and administration

- Employee benefits education and open enrollment support

Pro Tip: Ask any PEO you’re evaluating whether their technology platform includes a mobile app for employees. Adoption of benefits resources increases significantly when employees can access their information from their phone, which translates directly to fewer HR calls for your team.

How PEO-managed benefits affect retention and growth

This is where the numbers get compelling. Businesses using PEOs experience 10 to 14% lower voluntary employee turnover within 18 months, and they grow at a faster rate than comparable businesses managing HR independently. That is not a minor operational improvement. It represents real money and real momentum.

Turnover is expensive. Replacing a single employee typically costs 50 to 200% of their annual salary when you account for recruiting, training, and lost productivity. Employees with access to strong benefits are 32% more likely to stay compared to those with minimal coverage. PEO clients report recovering 70 to 90% of their historical turnover costs within 24 months of adoption. That recovery rate alone often justifies the investment.

Beyond core medical and retirement benefits, PEOs open the door to fringe benefits that most small businesses simply cannot offer independently. These supplementary benefits drive real satisfaction:

- Wellness programs and gym membership subsidies

- Employee Assistance Programs (EAPs) with mental health support

- Financial wellness tools and student loan repayment assistance

- Childcare support and backup care programs

- Telemedicine and virtual mental health services

These supplementary benefits move the needle on employee morale beyond what a pay raise alone can accomplish. Workers want to feel that their employer is invested in their whole life, not just their hours. A 20-person company that offers EAP access and telemedicine alongside competitive health insurance suddenly looks very attractive to candidates who might otherwise assume only large corporations can afford that kind of support.

The growth connection is direct too. Over 200,000 small and mid-sized businesses in the U.S. currently partner with PEOs, with 61% outsourcing health insurance administration and 50% outsourcing retirement plan management. The primary reason cited is the ability to stay focused on growth rather than HR complexity. When your leadership team is not spending time on benefits disputes and compliance questions, that time goes back into the business.

How to select a PEO that maximizes benefits access

Choosing the right PEO is where many small businesses stumble. The selection process can feel overwhelming when you are comparing dozens of providers across price, services, and technology. Here is a practical framework to make that process manageable.

-

Verify NAPEO membership. Choosing a NAPEO-affiliated PEO significantly reduces your risk. NAPEO membership signals financial stability, ethical standards compliance, and a commitment to ongoing industry education. It is the clearest quality filter available to you.

-

Evaluate the benefits plan menu. Ask for a full catalog of available health plans, carriers, and tier options. A quality PEO should offer multiple plan types, including HMO, PPO, and HDHP options, so you can match coverage to your workforce’s actual needs.

-

Assess their technology platform. Test the employee self-service portal yourself. Look for features like benefits comparison tools, digital enrollment, and mobile accessibility. These features directly affect whether your employees actually use and appreciate the benefits you offer.

-

Review compliance and administrative scope. Confirm exactly what the PEO covers. Some providers handle only payroll and basic HR. Others provide full-service benefits administration including ACA reporting, ERISA filings, and workers’ compensation. Know what is included before signing.

-

Understand the co-employment agreement. Review what control you retain over hiring decisions, compensation, and terminations. A reputable PEO will make clear that your employees remain yours in every meaningful operational sense.

Pro Tip: Working with a PEO broker, rather than going directly to a single provider, gives you access to multiple PEO options side by side. Brokers like Inclusive PEO Brokers do this matching work for you, saving significant time and often surfacing better pricing than you would find independently.

Common misconceptions about PEOs and benefits control

The biggest reason small businesses hesitate to explore PEOs is a set of persistent myths. Clearing these up makes the decision much easier.

-

“I’ll lose control of my employees.” Co-employment does not mean shared management. You retain full control over hiring, compensation, culture, and terminations. The PEO handles the administrative and compliance layer, not your workforce decisions.

-

“PEOs are just benefits brokers.” A broker sells you a plan. A PEO becomes an ongoing partner that manages enrollment, compliance, claims support, and regulatory reporting throughout the year. The two are structurally different.

-

“It will cost more than doing it ourselves.” The scale benefits, tax savings from Section 125 plans, and reduction in compliance errors almost always offset the PEO service fee. The average savings of $1,775 per employee per year demonstrates that the cost equation favors PEO partnership for most small businesses.

-

“Our company is too small.” PEOs work with businesses as small as five employees. Many are specifically designed for companies in the 10 to 150 employee range.

My honest take on PEO benefits after years in this space

I’ve had hundreds of conversations with small business owners who assumed competitive benefits were only possible once they hit some magic employee count, usually 50 or 100. That belief costs them talent every single year.

What I’ve learned is that the retention impact surprises people the most. It’s not the health plan alone that reduces turnover. It’s the signal the benefits package sends to employees. When a 15-person company offers telemedicine, an EAP, and a 401(k) with matching, employees notice. They feel valued. And that feeling is harder to replace than any single benefit line item.

What most people overlook when selecting a PEO is the quality of the employee-facing experience. Business owners focus on the pricing and the admin relief, which makes sense, but the platform employees interact with every day matters enormously. A clunky enrollment portal undermines the whole value proposition. I’ve seen companies switch PEOs not because of price but because their workforce couldn’t navigate the benefits tools.

My advice is this: don’t evaluate a PEO purely on your HR team’s experience. Put the employee portal in front of an actual employee during your due diligence. That test tells you more than any sales deck.

— John

How Inclusive PEO Brokers helps you find the right fit

If you’ve gotten this far and you’re wondering which PEO actually delivers on the benefits access and retention outcomes described above, that’s exactly the problem Inclusive PEO Brokers was built to solve.

Inclusive PEO Brokers works exclusively with small and mid-sized businesses to match them with PEOs that align with their specific workforce needs, industry requirements, and budget. The process is not about steering you toward a preferred vendor. It’s about filtering a crowded market down to the options that genuinely fit. Clients typically save 80 hours in the selection process and an average of $634 in associated costs. Inclusive has completed 133 successful implementations, with outcomes that include measurable improvements in benefits quality and employee retention.

Whether you’re exploring a PEO for the first time or looking to switch providers, the PEO selection process at Inclusive is structured to surface the right answers quickly. You can also explore Inclusive’s full approach to understand how the matchmaking and implementation process works from start to finish.

FAQ

What does a PEO do to improve employee benefits?

A PEO pools your employees with thousands of workers across multiple businesses, giving your company access to large-group health insurance rates and plan types that most small businesses cannot access on their own. The PEO also manages enrollment, compliance reporting, and claims support so your team is not handling that administrative work.

How much can a small business save by using a PEO for benefits?

PEO clients save an average of $1,775 per employee per year, representing a 27% ROI when accounting for benefits cost savings, reduced administrative overhead, and lower compliance risk.

Does a PEO take control away from the employer?

No. The co-employment model means the PEO handles HR administration and compliance, but you retain full authority over hiring, compensation, culture, and day-to-day management. Your employees remain yours in every operational sense.

What benefits can a PEO typically offer that small businesses can’t get alone?

PEOs commonly provide access to multiple health plan tiers, 401(k) plans with employer match options, dental and vision coverage, EAPs, telemedicine, wellness programs, and financial wellness tools. Many of these are either unavailable or cost-prohibitive for small businesses purchasing independently.

How do I know if a PEO is reputable?

Look for NAPEO membership as your first filter. NAPEO-affiliated PEOs meet standards for financial stability and compliance. Working with a PEO broker who vets providers on your behalf adds another layer of protection and saves significant research time.

Recommended

.svg)

Seeking a different solution? Meet Your Business Needs