.png)

Why Small Businesses Struggle with Benefits in 2026

Small businesses struggle with employee benefits primarily because structural constraints, including thin profit margins, limited administrative capacity, and unpredictable revenue, prevent them from matching the coverage depth and cost-sharing that larger employers provide. This gap is not a matter of willingness. It is a matter of architecture. The formal term for this disparity is the “small business employee benefits gap,” a concept well-documented by researchers at the Urban Institute and policy analysts at KFF. Understanding why this gap exists, and what it actually costs your business in talent and retention, is the first step toward doing something about it.

Why small businesses struggle with benefits: the structural reality

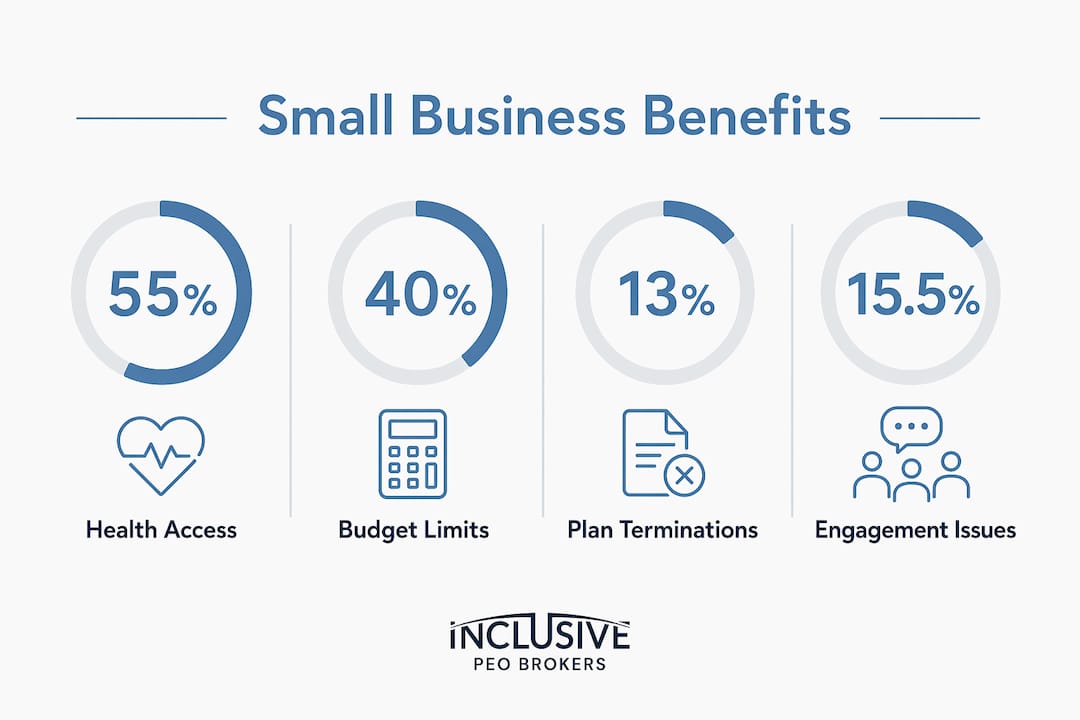

The core reason why benefits are hard for small firms comes down to economics and scale. Workers at smaller firms have only 55% access to health benefits, compared to 88% at larger firms, with dental access at 27% versus 59% and retirement or financial planning access at 14% versus 39%. These numbers reflect a structural divide, not a motivation gap. Larger employers spread fixed administrative and insurance costs across hundreds or thousands of employees, which drives down per-person pricing. Your business, with 10 or 20 employees, simply cannot access the same pricing tiers.

Budget pressure compounds the problem directly. 40% of small and mid-sized businesses cite limited budgets as a major barrier to offering benefits, and 37% point to rising benefits costs specifically. That means benefits spending competes with payroll, equipment, rent, and every other operating line. When revenue dips unexpectedly, benefits are often the first area where owners look for relief, which creates instability in your offerings and erodes employee trust over time.

Volatile revenue is a particularly underappreciated obstacle. Large corporations can absorb a bad quarter without cutting health coverage. A 12-person professional services firm cannot always say the same. Long-term benefits planning requires predictable cash flow, and many small businesses simply do not have that consistency, especially in their first five years.

| Challenge | Impact on small businesses |

|---|---|

| Limited budget | Fewer plan options, lower employer contribution rates |

| Volatile revenue | Difficulty committing to multi-year benefit structures |

| Small employee pool | Higher per-person insurance premiums |

| Thin admin capacity | Renewal and compliance tasks fall on non-specialists |

Pro Tip: Before shopping for benefits, calculate your total annual benefits budget as a percentage of payroll. Most small businesses that successfully offer competitive packages allocate between 15% and 30% of total compensation costs to benefits, which gives you a realistic ceiling before you start comparing plans.

How does benefits administration complexity affect small firms?

Administration is where the challenges in offering benefits become most visible day-to-day. Managing employee benefits is not a single task. It involves health insurance, dental, vision, retirement plans, life insurance, disability coverage, and sometimes voluntary perks like commuter benefits or wellness stipends. Each category has its own vendor, renewal cycle, compliance requirement, and invoice. For a small HR team, or a business owner wearing multiple hats, this is genuinely overwhelming.

HR teams at small firms face concentrated pressure around annual renewals, where they must evaluate new plan options, reconcile invoices, coordinate with vendors, and communicate changes to employees, all within a compressed window. This leaves almost no time for strategic thinking about whether the current benefits mix actually serves your workforce. The result is that most small businesses renew what they had last year, even when better or more affordable options exist.

Hidden costs make this worse. Unexpected retirement plan fees cause 13% of employers to terminate their plans entirely and push 26% to reduce their matching contributions. These are not edge cases. They represent a pattern where small employers enter benefit arrangements without fully understanding the fee structures, then face a difficult choice between absorbing the cost or cutting the benefit.

The administrative complexity of benefits management crowds out strategic decision-making for small business HR teams. When your time is consumed by invoice reconciliation and vendor calls, you are not analyzing whether your benefits package is actually helping you recruit or retain people. That disconnect between effort and outcome is one of the most frustrating aspects of managing benefits as a small employer.

Pro Tip: Ask every benefits vendor for a complete fee disclosure document before signing. Request both the base premium and any administrative, platform, or compliance fees. Comparing total cost of ownership, not just the monthly premium, prevents the hidden-fee surprises that derail small business retirement and health plans.

Why do employee engagement and utilization challenges worsen the problem?

Offering a benefit and having employees actually use and value it are two different outcomes. Benefits access does not always translate to value when employee premium burdens are high or communication and engagement are poor. This is the engagement gap, and it quietly erodes the return on every dollar you invest in your benefits package.

The premium contribution problem is especially acute for family coverage. 29% of covered workers at small firms must contribute more than 50% of premiums for family coverage, compared to just 5% at large firms. When an employee has to pay the majority of a family health plan out of pocket, they may decline coverage entirely, which means your investment in offering that plan produces no retention benefit at all.

Here are four specific ways the engagement gap damages small business benefits ROI:

- Low enrollment rates. When employee premium shares are high, workers opt out, leaving your plan with fewer participants and potentially higher per-person costs in the following renewal cycle.

- Misaligned plan design. Benefits chosen without surveying employees often miss the mark. A workforce of young parents needs different coverage than a team of recent graduates, and a one-size plan satisfies neither group fully.

- Poor communication at open enrollment. Many small businesses send a single email about benefits changes and consider the job done. Employees who do not understand their options default to inaction, which means they may stay on suboptimal plans for years.

- Underutilized voluntary benefits. Voluntary options like dental, vision, or life insurance add perceived value at low cost to the employer, but only if employees know they exist and understand how to use them.

15.5% of organizations report engagement, communication, or take-up as a top benefits challenge. For small businesses without a dedicated HR communications function, this number is almost certainly higher in practice.

How do small businesses compare to larger companies in benefits access?

The gap between small and large firm benefits is not marginal. It is structural and measurable across every major benefit category. The data from the Urban Institute and KFF paints a consistent picture: employees at small firms receive less coverage, pay more for what they do receive, and have access to fewer plan types.

| Metric | Small firms (≤50 employees) | Large firms (≥100 employees) |

|---|---|---|

| Health benefits access | 55% | 88% |

| Dental benefits access | 27% | 59% |

| Retirement/financial planning access | 14% | 39% |

| Workers contributing >50% of family premium | 29% | 5% |

The employer contribution gap is particularly significant for recruitment. When a candidate compares your offer to one from a 500-person company, they are not just comparing salary. They are comparing the total compensation package, including how much of their health premium you cover. Employer-sponsored health insurance reaches 60% of lower-paid workers versus 80% overall, which means the access problem is most severe for exactly the workers small businesses most often hire.

This disparity has a direct talent consequence. Your ability to recruit experienced professionals and retain your best performers is constrained when your benefits package cannot compete with what larger employers offer. The solution is not necessarily to match large-firm spending dollar for dollar. It is to close the gap strategically by using the right tools and partnerships.

What practical approaches can help small businesses improve their benefits?

Small businesses do not need to outspend large employers to compete on benefits. They need to spend more intentionally and use structures that give them access to group-level pricing and administrative support.

- Professional Employer Organizations (PEOs). A PEO operates under a co-employment model, where your employees are jointly employed by your business and the PEO. This allows your team to access large-group health insurance rates, retirement plans, and compliance support that would otherwise be unavailable at your firm’s size. Working with an employee benefits broker who specializes in PEO matching can help you find the right fit without spending months evaluating vendors on your own.

- ICHRA and QSEHRA models. Individual Coverage Health Reimbursement Arrangements (ICHRAs) and Qualified Small Employer HRAs (QSEHRAs) allow you to reimburse employees for individual health insurance premiums rather than sponsoring a group plan. ICHRA vs QSEHRA distinctions matter for eligibility and contribution limits, so understanding the regulatory differences before choosing a model prevents costly compliance pivots later.

- Voluntary benefits. Dental, vision, life insurance, and disability coverage offered on a voluntary basis cost the employer little or nothing while expanding the perceived value of your total package. Employees pay group rates they could not access individually.

- Pooled purchasing arrangements. Industry associations and chambers of commerce sometimes offer group purchasing pools for health insurance. These are worth investigating before going directly to an insurer, as they can provide pricing closer to large-group rates.

- Transparent fee structures. When evaluating any benefits vendor, require a full breakdown of administrative, compliance, and platform fees upfront. Reviewing retirement plan costs with this level of scrutiny prevents the hidden-fee problem that forces 13% of small employers to terminate their plans.

Key takeaways

Small businesses struggle with benefits because structural constraints, not lack of effort, create persistent gaps in access, affordability, and administration that require deliberate strategy to close.

| Point | Details |

|---|---|

| Access gap is measurable | Workers at small firms have 55% health benefits access versus 88% at large firms. |

| Budget and cost pressure dominate | 40% of small businesses cite limited budgets and 37% cite rising costs as primary barriers. |

| Premium burden reduces utilization | 29% of small-firm workers pay over half of family premiums, cutting enrollment and perceived value. |

| Administration complexity crowds out strategy | Hidden fees and renewal pressure leave small HR teams with no time for plan optimization. |

| PEOs and HRAs close the gap | Co-employment models and reimbursement arrangements give small firms access to large-group pricing and support. |

The uncomfortable truth about small business benefits

I have worked with enough small business owners to know that the benefits conversation almost always starts the same way: “We want to offer something, but we just can’t afford it.” What I have found, though, is that affordability is rarely the only issue. The deeper problem is that most small business owners are making benefits decisions reactively, under time pressure, without a clear picture of what their employees actually need or value.

The businesses that successfully close the benefits gap are not necessarily spending more. They are spending differently. They have separated the administrative work from the strategic work, often by partnering with a PEO or a specialized broker who handles the complexity, so the owner can focus on plan design and employee communication. They survey their teams before open enrollment. They choose two or three benefits that genuinely matter to their workforce rather than trying to offer everything at a mediocre level.

The other thing I would push back on is the assumption that you have to solve this alone. Executive consulting support and PEO partnerships exist precisely because benefits administration is a specialized function that most small businesses cannot staff internally. Using expert support is not an admission of weakness. It is the same logic that leads you to hire an accountant instead of doing your own taxes.

Start with what your employees actually want. Build from there with the right partners. The gap is real, but it is not permanent.

— John

How Inclusive PEO Brokers helps small businesses tackle benefits challenges

If the structural and administrative barriers described in this article feel familiar, you are not alone. Inclusive PEO Brokers works specifically with small and medium-sized businesses to match them with the right Professional Employer Organization, cutting through the complexity so you can access better benefits at lower cost.

Inclusive PEO Brokers has completed 133 successful PEO implementations, saving clients an average of 80 hours in the selection process and $634 in costs. Their PEO matching process filters options based on your specific workforce size, industry, and benefits goals, so you are not evaluating dozens of vendors that were never the right fit. If you are ready to give your team access to large-group benefits without the administrative burden, explore Inclusive PEO Brokers to find the right solution for your business.

FAQ

Why do small businesses struggle to offer health insurance?

Small businesses face higher per-person insurance premiums because they cannot spread costs across a large employee pool, and workers at small firms have only 55% access to health benefits compared to 88% at large firms. Limited budgets and volatile revenue make it difficult to commit to consistent employer contributions.

What percentage of small business employees lack retirement benefits?

Only 14% of workers at small firms have access to retirement or financial planning benefits, compared to 39% at large firms, according to Urban Institute research. Hidden administrative fees compound the problem, with 13% of small employers terminating retirement plans due to unexpected fee overruns.

How can a PEO help a small business offer better benefits?

A PEO uses a co-employment model to pool your employees with those of other small businesses, giving your team access to large-group health insurance rates and retirement plans. This structure reduces both the cost and the administrative burden of managing employee benefits without requiring you to build an internal HR department.

What is the difference between ICHRA and QSEHRA for small businesses?

An ICHRA (Individual Coverage Health Reimbursement Arrangement) has no contribution limits and can be offered alongside group plans, while a QSEHRA (Qualified Small Employer HRA) is limited to businesses with fewer than 50 employees and caps annual reimbursements. Choosing the wrong model can trigger compliance issues, so reviewing ICHRA vs QSEHRA rules before implementation is critical.

Why do employees at small firms pay more for family health coverage?

29% of covered workers at small firms contribute more than 50% of family health premiums, compared to just 5% at large firms. This high employee cost share reduces plan enrollment and diminishes the retention value of the benefit, even when the employer is making a genuine effort to offer coverage.

Recommended

.svg)

Seeking a different solution? Meet Your Business Needs